2025-051 The February 2025 Bar Exam

The State Bar’s Poor Implementation of Changes to the Exam Negatively Affected Test Takers

Published: July 9, 2026Report Number: 2025-051

July 9, 2026

2025-051

The Governor of California

President pro Tempore of the Senate

Speaker of the Assembly

State Capitol

Sacramento, CA 95814

Dear Governor and Legislative Leaders:

As required by Business and Professions Code section 6145, subdivision (d), my office conducted an audit of the State Bar of California (State Bar) and its administration of the California Bar Examination administered in February 2025 (February 2025 bar exam). In general, we determined that the State Bar poorly implemented certain changes to the bar exam, which had a negative effect on test takers.

In part to reduce costs and address the solvency of its Admissions Fund, the State Bar decided in 2024 to switch from administering the bar exam in person to offering test takers the option to take the bar exam remotely or in person. To make this switch, the State Bar contracted with Kaplan Exam Services, LLC (Kaplan) to develop multiple-choice questions for the bar exam. However, the State Bar did not specify to Kaplan certain legal topics required for the bar exam, and the State Bar asked another of its vendors, ACS Ventures, LLC (ACS Ventures) to develop additional exam questions, which it did using artificial intelligence. Although the State Bar engaged in a content validation process to review, edit, and validate all the newly developed multiple-choice questions, the State Bar’s execution of this process had flaws that hindered its effectiveness.

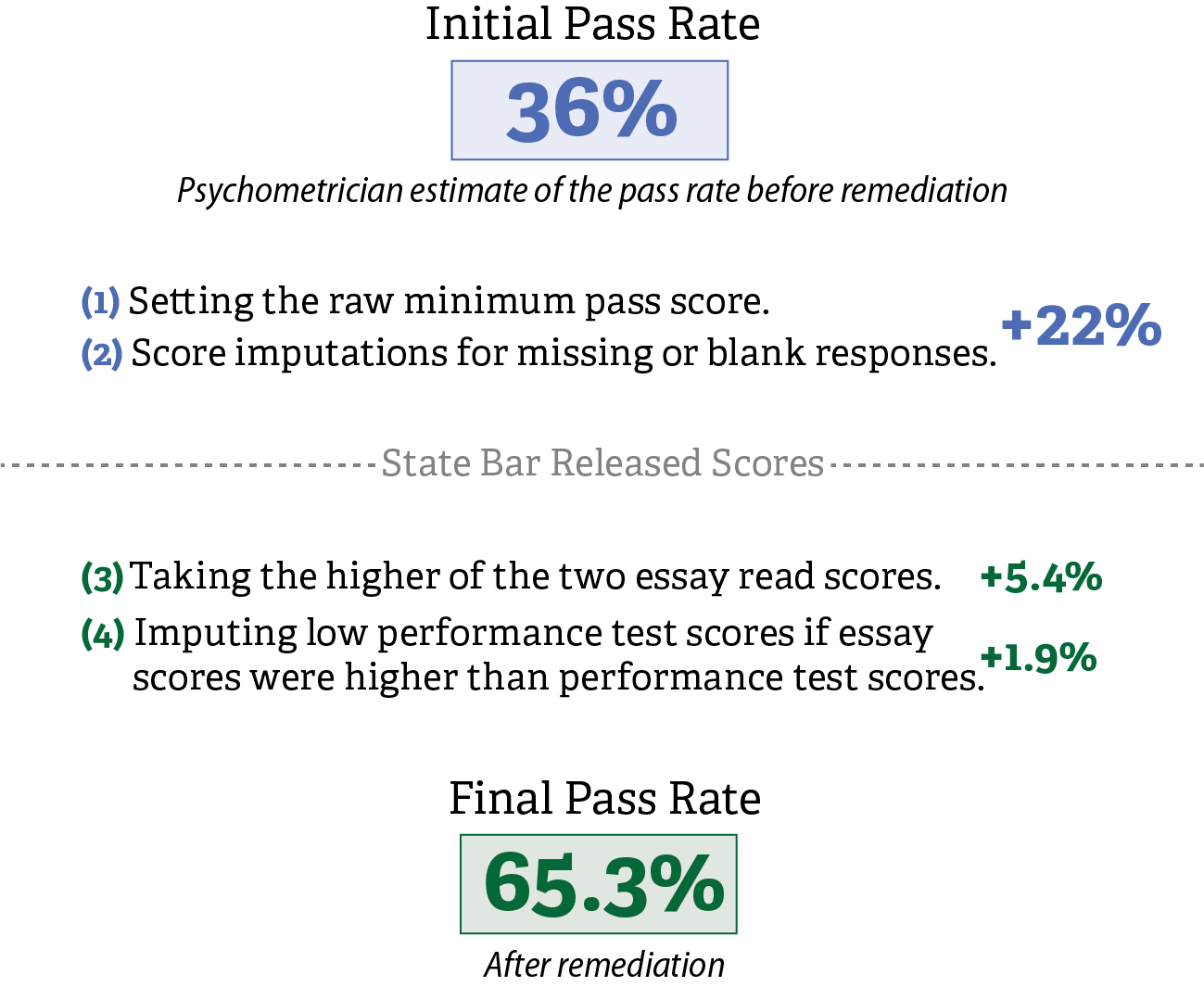

The State Bar also contracted with ProctorU Inc., dba Meazure Learning (Meazure Learning), to administer the February 2025 bar exam without first defining business requirements or establishing criteria to evaluate the vendor’s performance. It also contracted with Meazure Learning despite knowing that it lacked an important tool to administer the exam’s performance test portion. Further, the State Bar did not ensure that Meazure Learning addressed the causes of computer freezes, crashes, and error messages that test takers faced during a November 2024 pretest. The technical and administrative problems that test takers experienced caused the State Bar to raise its pass rate from about 36 percent of test takers to about 65 percent of test takers of the February 2025 bar exam.

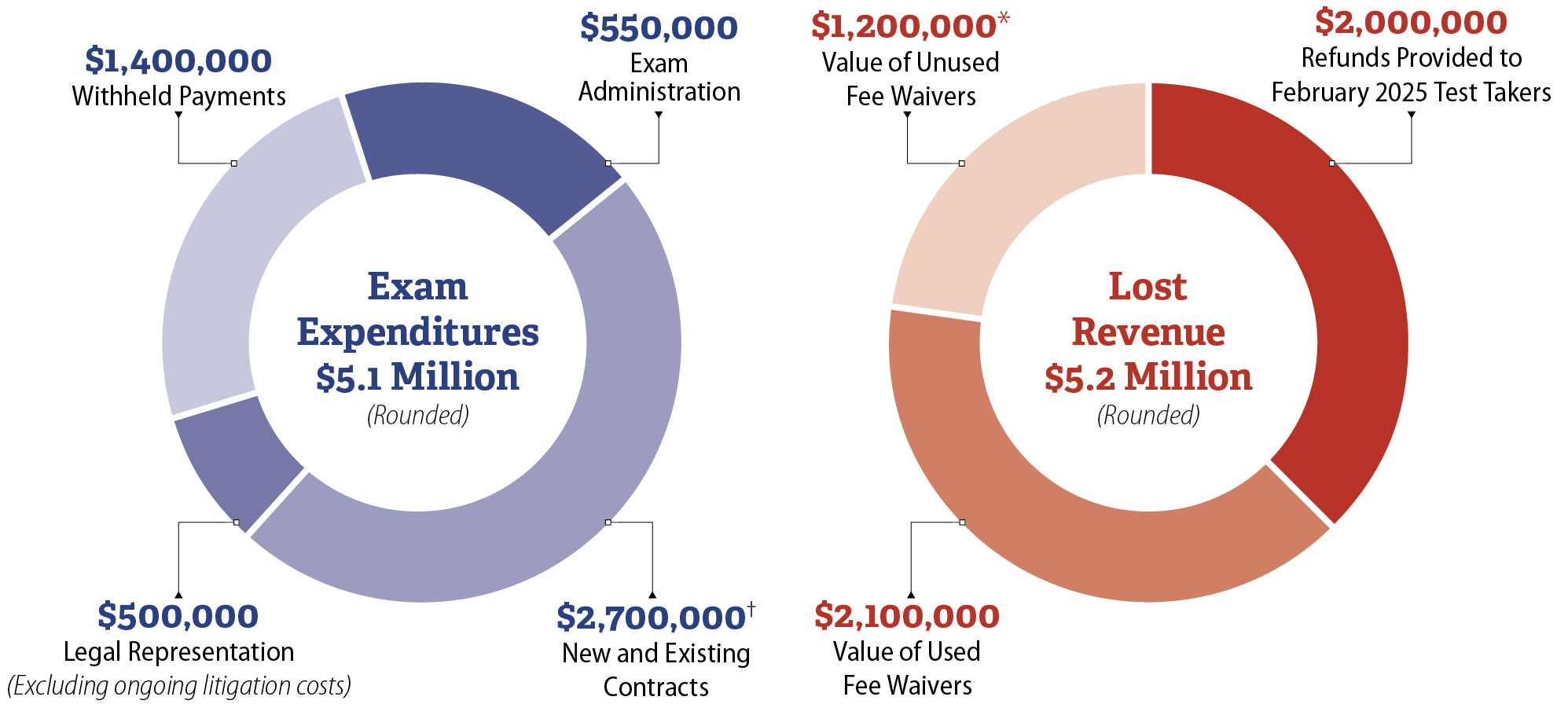

The State Bar did not achieve cost savings in its administration of the February 2025 bar exam, which will cost at least $5.1 million, not including the costs of pending legal matters, and it experienced at least $4 million in lost revenue from the remedies it provided to February 2025 test takers, which included exam refunds and fee waivers.

Respectfully submitted,

GRANT PARKS

California State Auditor

Selected Abbreviations Used in This Report

| AI | artificial intelligence |

| CALS | California Accredited Law Schools |

| IT | information technology |

| NCBE | National Conference of Bar Examiners |

| RFI | Request for information |

Summary

Key Findings and Recommendations

One of the key responsibilities of the State Bar of California (State Bar) is the biannual administration of the California Bar Examination (bar exam). Before the COVID-19 pandemic, individuals seeking to practice law in California had to take the bar exam in person. However, after offering the bar exam remotely during the pandemic, the State Bar decided in 2024 to use a hybrid model to administer the exam in February 2025 (February 2025 bar exam). This model allows test takers to take the exam either in person or remotely. By offering the remote option, the State Bar hoped to reduce the cost of administering the bar exam and thus address the impending insolvency of its Admissions Fund, which it uses to support activities, such as examinations, pertaining to admission to the practice of law.

Administered over a two-day period, the bar exam is composed of two sections: a written section with essay questions and a performance test question, and a section with multiple-choice questions. Historically, the State Bar used multiple-choice questions from the National Conference of Bar Examiners (NCBE), but the NCBE does not allow for remote administration of its exam materials. To address this issue, the State Bar retained the services of Kaplan Exam Services, LLC (Kaplan) to develop multiple-choice questions. It also contracted with ProctorU Inc., dba Meazure Learning (Meazure Learning), to provide exam administration services and used its preexisting contractual relationship with ACS Ventures, LLC (ACS Ventures) to provide psychometric consulting services and analysis.1 2

Ultimately, a significant portion of the 4,200 individuals who took the February 2025 bar exam experienced problems. To better understand why these problems occurred, the Legislature and Governor of California amended state law to require our office to perform an audit of the State Bar’s efforts to administer the February 2025 bar exam.

The State Bar’s Timeline and Poor Planning Created Challenges With Question Development

The State Bar’s procurement efforts resulted in insufficient time for Kaplan to develop questions that covered all required exam topics. The State Bar initiated its search for a contractor 13 months before the February 2025 bar exam. However, because of delays in that process, it did not enter into a written agreement with Kaplan until August 2024, leaving only six months for Kaplan to develop questions and for the State Bar to validate them. The State Bar’s contract with Kaplan also did not specify the topics needed for the February 2025 bar exam. Thus, the questions Kaplan eventually developed did not cover certain important legal topics required for the exam. To address this issue, the State Bar asked ACS Ventures—its contractor for psychometric services—to develop exam questions for the missing topic areas. Although the State Bar admissions office was aware that ACS Ventures would develop these questions by using artificial intelligence (AI), the office did not communicate this information to the State Bar’s executive leadership.

Question Issues Forced the State Bar to Remove More Questions From Scoring Than It Had Intended

The State Bar engaged in a content validation process to review and edit the newly developed multiple-choice questions it used on the February 2025 bar exam, with the goal of ensuring their appropriateness and accuracy. In this process, content validation panels and a subject matter expert performed reviews of the bar exam’s multiple-choice questions. However, the State Bar’s execution of its content validation process had flaws that hindered its effectiveness. For example, the State Bar directed a single subject matter expert to review all 200 questions, rather than following the NCBE’s approach of hiring subject matter experts in each of the legal subjects the exam covered. Consequently, after the February 2025 bar exam, ACS Ventures identified 40 of the exam’s 200 multiple‑choice questions, or 20 percent, that had performance issues such as questions that did not effectively differentiate test takers’ performance. The State Bar ultimately included 19 of these questions among those it scored for the exam. Although the State Bar had planned to remove 25 of the 200 questions—consistent with NCBE’s approach—the State Bar identified four additional questions with potential legal accuracy issues, which resulted in the State Bar removing 29 questions from the February 2025 bar exam.

The State Bar Contracted With Meazure Learning Without Fully Verifying Its Ability to Effectively Administer the February 2025 Bar Exam

The State Bar selected Meazure Learning to administer the February 2025 bar exam without first defining the State Bar’s exam administration requirements, such as the functionality to remotely administer the materials for the performance test. Instead, the State Bar largely relied on Meazure Learning’s assertions that it had the necessary capabilities. Although the State Bar took some steps to assess Meazure Learning’s remote platform and test centers, it did not verify that Meazure Learning corrected the problems it identified in its assessment. If the State Bar had clearly identified its business requirements, it could have taken steps to ensure that its contract with Meazure Learning identified benchmarks Meazure Learning needed to meet and dates by which Meazure Learning needed to demonstrate specific capabilities. For example, the Statewide Information Management Manual recommends as a best practice that agencies include in their contracts requirements that identify project deliverables and milestones required for project completion that are specific, unambiguous, testable, and traceable. Further, the State Bar did not promptly address Meazure Learning’s known inability to provide a highlighting tool necessary to administer the performance portion of the exam, despite knowing that it would be the hardest portion to administer remotely. Finally, the State Bar did not ensure that testing locations were a reasonable distance from test takers’ homes, nor did it provide specific information to test takers about which in-person testing locations were available until a month before the exam.

The State Bar Fell Short of Preventing the Technical and Administrative Failures That Occurred in the February 2025 Bar Exam

The State Bar failed to prevent issues test takers experienced with the administration of the February 2025 bar exam. For example, it did not ensure that Meazure Learning addressed the causes of freezes, crashes, and error messages that test takers faced during a pretest in November 2024. In the same November pretest, many participants reported that Meazure Learning’s proctors did not understand or inconsistently enforced exam rules. Nonetheless, the State Bar did not take adequate action to ensure that Meazure Learning better trained its proctors before the February 2025 bar exam. As a result, about half of the survey respondents who took the February 2025 bar exam reported experiencing similar problems. Because of the technical and administrative problems that test takers experienced, the State Bar made significant adjustments to its scoring for the February 2025 bar exam, which raised its pass rate from about 36 percent of test takers to about 65 percent of test takers.

The State Bar Experienced No Cost Savings on the February 2025 Bar Exam and at Least $4 Million in Revenue Losses

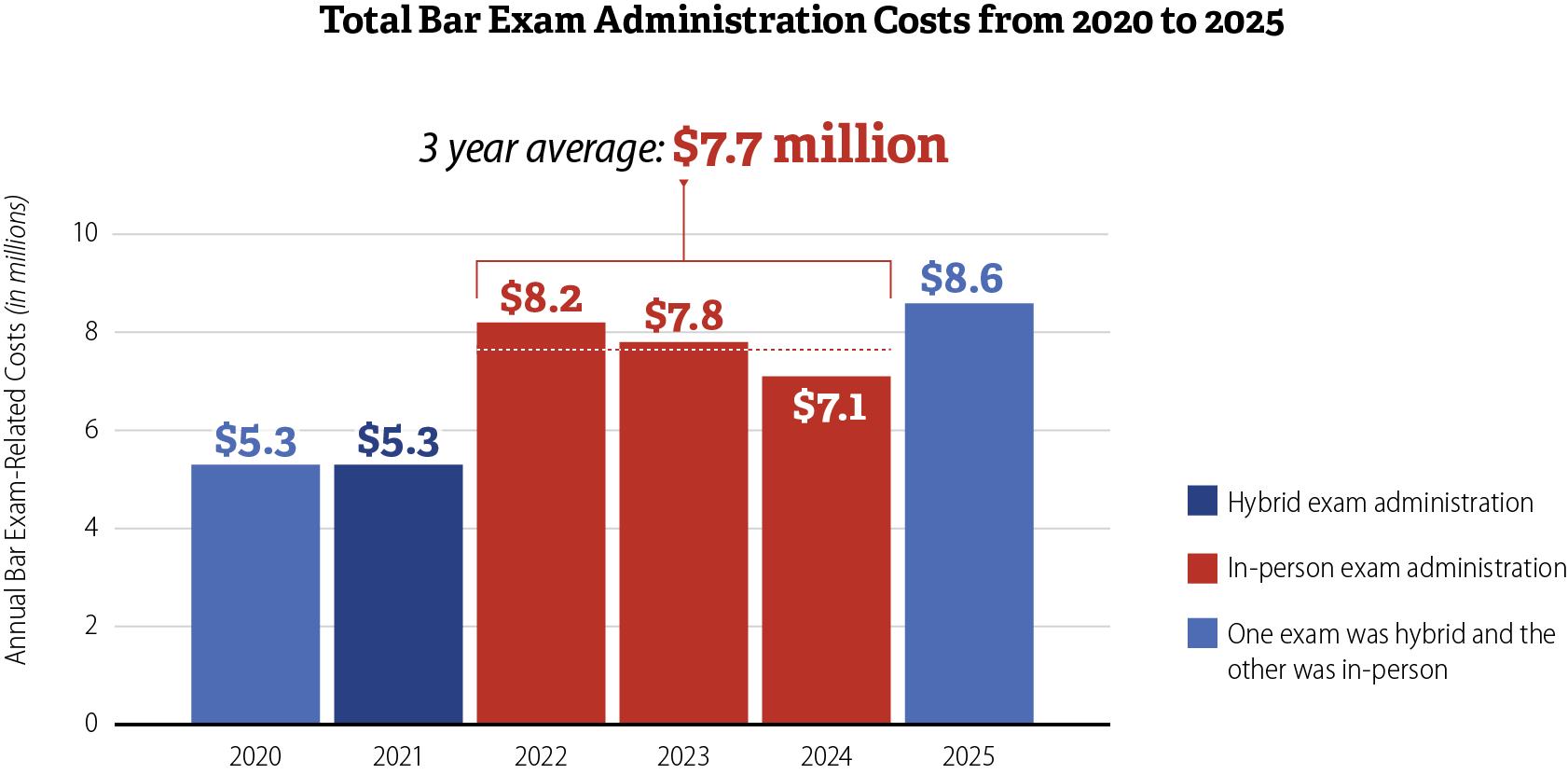

Despite its intent to reduce bar exam expenses, the State Bar did not achieve cost savings in its administration of the February 2025 bar exam. From 2022 to 2024, the State Bar spent an average of $7.7 million annually on bar exams. The February 2025 bar exam alone has cost the State Bar $5.1 million, not including the costs of pending legal matters. In addition, the State Bar experienced at least $4 million in lost revenue as a result of remedies it provided to February 2025 test takers, including exam refunds and fee waivers. The State Bar has increased certain fees in an effort to cover these costs and to keep the Admissions Fund solvent through 2028. Moreover, the State Bar has evaluated bar exam options to assess and identify the future of the bar exam to help ensure that the State Bar avoids the problems that led to and that occurred during the February 2025 bar exam.

In several instances we found that the State Bar had already taken steps to address concerns with the February 2025 bar exam. However, to improve the quality of its multiple-choice questions, we recommend that the State Bar implement a standardized review process for multiple-choice questions. We also make several other recommendations. For instance, we recommend that the State Bar revise its contracting policies to require managerial approval of any requests for vendor actions outside the scope of contracted responsibilities. Also, to reduce the risk and perception of bias during the question development, validation, and scoring processes, we recommend that the State Bar implement controls that require separation of contractor responsibilities across different stages of exam development, including independent review and approval, and formal oversight of contractors that perform multiple roles.

Agency Comments

The State Bar agreed with all of the report’s recommendations and described efforts it has already begun to implement them. It also indicated that the Supreme Court of California (Supreme Court) is currently considering the State Bar’s recommendation to adopt the NCBE’s NextGen Uniform Bar Exam for implementation in July 2028, which if adopted by the Supreme Court, may reduce the applicability of some of our recommendations.

Introduction

Background

The State Bar is a public corporation established by the California Constitution. Its mission is to protect the public by licensing, regulating, and disciplining attorneys. One of its key responsibilities is the administration of the bar exam. State law requires anyone seeking a license to practice law in California to pass the two-day bar exam. The bar exam’s purpose is to ensure that attorneys who pass possess at least the minimum competency to practice law in the State. Licensure exams like the bar exam distinguish candidates who are at least minimally competent from those who are not competent and could harm the public.

Individuals who take the bar exam may study for months before the exam after having invested a considerable amount of time and money in attending law school. Nevertheless, test takers taking the February 2025 bar exam experienced technical and exam administration problems that could have created barriers to their ability to pass the exam and practice law. In fact, even before the exam began, test takers struggled to book their testing sites because the State Bar did not clearly communicate about testing locations. Media reports indicate that during the exam, the testing platform repeatedly crashed; one test taker stated that he had to start the exam more than 30 times. Media reports also note that test takers experienced screen lagging, error messages, and problems with the copy-and-paste tools. The State Bar acknowledged that myriad problems occurred, and as a result, it offered refunds totaling $2 million for the February 2025 bar exams, and the State Bar Board of Trustees (Board) approved $4.9 million in fee waivers for use on the July 2025, February 2026, or July 2026 bar exams.

Because of the problems with the exam, the Legislature and the Governor of California amended state law to require our office to perform an audit of the State Bar’s administration of the February 2025 bar exam. Specifically, state law requires us to evaluate the State Bar’s bidding and contracting process for the February 2025 bar exam, the process it used to administer the exam, the use of AI to create multiple‑choice questions, and the anticipated and actual costs arising from this bar exam.

The State Bar’s and Supreme Court’s Responsibilities Related to the Bar Exam

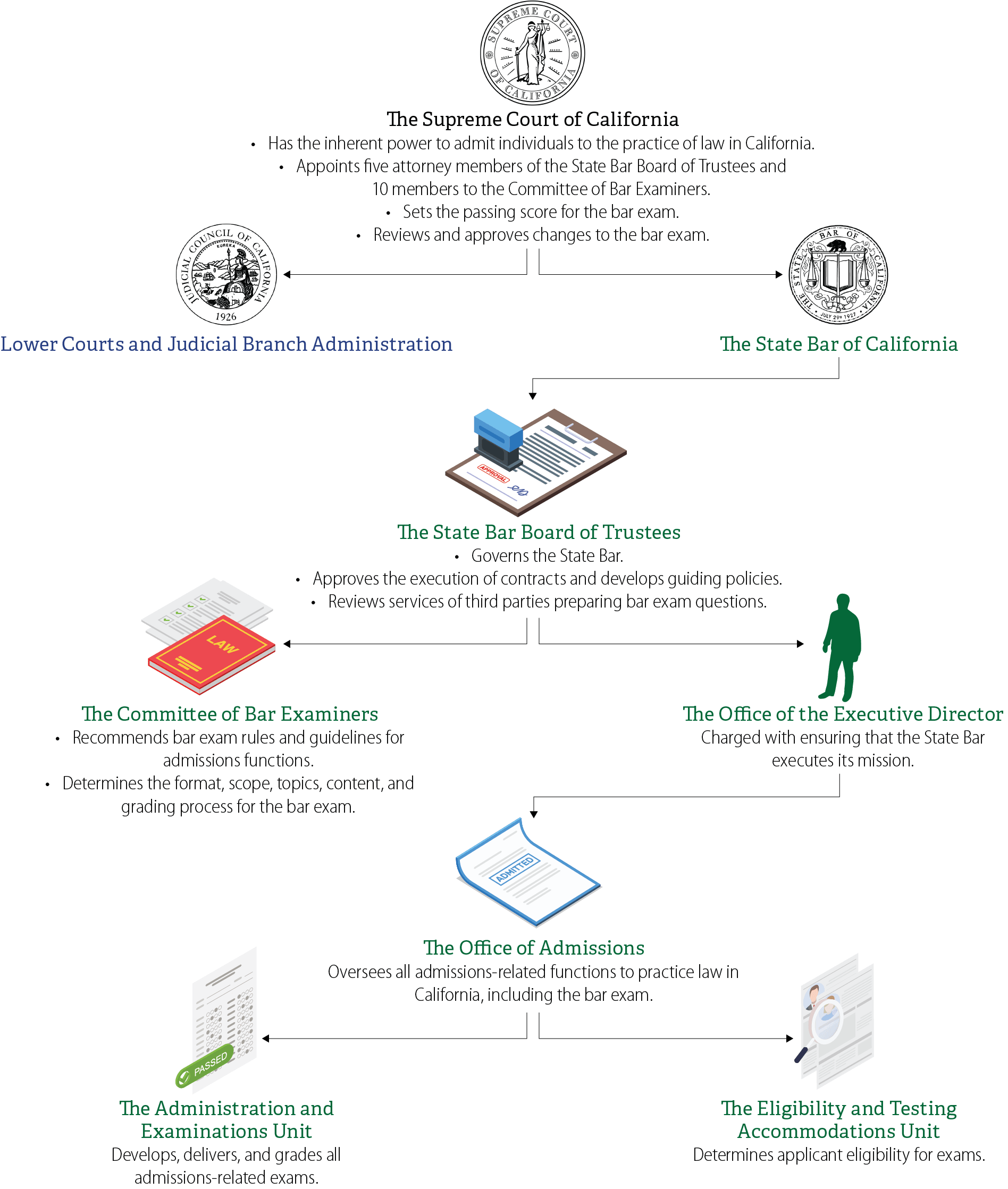

As Figure 1 illustrates, two entities governed by the Board—the Committee of Bar Examiners (Committee) and the Office of the Executive Director—were responsible for developing, administering, and scoring the February 2025 bar exam. In 2025, the Office of the Executive Director had a budget of $1.8 million with five full-time positions. The Office of Admissions (admissions office)—under the authority of the executive director—had a budget of $28.8 million and about 68 full-time positions.

Figure 1

The Authority Over the Administration of the February 2025 California Bar Exam

A flow chart that outlines hierarchically the entities that had responsibility over the administration of the February 2025 California bar exam. These entities are:

The Supreme Court of California

The Supreme Court oversees the lower courts and judicial branch administration, including the State Bar of California. The Supreme Court has the power to admit individuals to the practice of law in California. It appoints 5 attorney members to the State Bar Board of Trustees and 10 members to the Committee of Bar Examiners. It sets the passing score for the bar exam and reviews and approves changes to the bar exam.

Lower Courts and Judicial Branch Administration

The State Bar of California

The State Bar Board of Trustees

The Board governs the State Bar, approves the execution of contracts, develops guiding policies, and reviews services of third parties preparing bar exam questions.

The Committee of Bar Examiners

The Committee recommends bar exam rules and guidelines for admissions functions. It also determines the format, scope, topics, content, and grading process for the bar exam.

The Office of the Executive Director

The executive director is charged with ensuring that the State Bar executes its mission.

The Office of Admissions

The Office of Admissions oversees all admissions-related functions to practice law in California, including the bar exam.

The Administration and Examinations Unit

This unit develops, delivers, and grades all admissions-related exams.

The Eligibility and Testing Accommodations Unit

This unit determines applicant eligibility for exams.

Source: State law, California Rules of Court, and State Bar website.

Although the State Bar has numerous duties related to the bar exam, the Supreme Court has the ultimate authority to admit individuals to practice law in California. It also appoints some members of both the Board and the Committee and sets the passing score for the bar exam. Significant changes to the bar exam require Supreme Court approval.

Administration of Bar Exams Before February 2025

The State Bar administers the bar exam twice a year, in February and July.3 Each exam consists of two sections: a written section with essay questions and a performance test question, and a section with multiple-choice questions. The text box describes each of these sections in more detail. The State Bar uses different questions for each administration of the bar exam. It then uses a process called equating to ensure that the multiple-choice score on one exam administration demonstrates equivalent proficiency to another exam administration. The State Bar uses another process called scaling to ensure that any variation in the difficulty of the written section across exam administrations does not affect a test taker’s likelihood of passing.

Essays and Performance Test

50% of total bar exam score

- Five 1-hour essay questions that may be about any of the following topics:

- Business Associations

- Civil Procedure

- Community Property

- Constitutional Law

- Contracts

- Criminal Law and Procedure

- Evidence

- Professional Responsibility

- Real Property

- Remedies

- Torts

- Trusts

- Wills and Succession

- One 90-minute performance test question

- Evaluates examinees’ ability to review select source documents to complete a task in a thorough and organized manner.

Multistate Bar Examination

50% of total bar exam score

- 200 multiple-choice questions that test seven subjects:

- Civil Procedure

- Constitutional Law

- Contracts

- Criminal Law and Procedure

- Evidence

- Real Property

- Torts

Source: State Bar website.

Before the February 2025 bar exam, the State Bar followed a consistent process when selecting or developing the exam questions it used. Specifically, the admissions principal program analyst explained that law professors draft essay questions and performance test questions. The State Bar retains practicing attorneys to develop and grade essay and performance test questions, and the State Bar presents them to the Committee for approval for inclusion in a bar exam. The State Bar pretests essay and performance test questions to identify problems like ambiguity, bias, and the degree of difficulty.

For the multiple-choice section of the bar exam, the State Bar historically used the questions from the NCBE. A nonprofit corporation, the NCBE develops and licenses the Multistate Bar Examination, the purpose of which is to assess the extent to which a test taker can apply fundamental legal principles and legal reasoning to analyze given fact patterns. The NCBE does not allow for remote administration of exams that use its materials, although it made exceptions in 2020 and 2021 because of the pandemic. During that time, the State Bar generally administered its October 2020, February 2021, and July 2021 bar exams remotely.

For these three exams, the State Bar contracted with ExamSoft Worldwide, Inc. (ExamSoft) to provide exam software and proctoring services. ExamSoft recorded test takers as they took the bar exam, and State Bar staff reviewed the recordings of test takers after the exam to identify possible instances of cheating or other violations of exam rules. The chief of the admissions office noted that the State Bar had to review thousands of recordings after those three exams and found that the technology was not adequate to ensure the integrity of the exam. Therefore, the State Bar was not willing to use the technology again in 2025.

The State Bar’s Changes to the February 2025 Bar Exam

For at least five years prior to the February 2025 bar exam, the State Bar considered making changes to the bar exam. To explore potential changes to the content and format of the bar exam, in 2020, the Supreme Court and the Board established the Blue Ribbon Commission on the Future of the Bar Exam (Blue Ribbon Commission) to make recommendations regarding the bar exam’s content and format. The Board received the Blue Ribbon Commission report in May 2023. The report recommended that California develop its own exam rather than relying on the NCBE. The Blue Ribbon Commission’s arguments in favor of this recommendation included providing California with flexibility related to exam delivery and frequency. The Supreme Court adopted, with modifications, most of the report’s recommendations in October 2024.

While the State Bar was exploring changes to the bar exam, its Admissions Fund developed a deficit. The Admissions Fund supports activities, such as examinations, pertaining to admission to the practice of law. In 2023, the State Bar conducted a fee analysis to address the deficit and proposed substantial increases to most fees applicants pay, as well as fees charged to law schools. Accordingly, the Board voted in September 2023 to increase admissions fees; however, even with those adjustments, the State Bar still projected that the Admissions Fund would be insolvent by the end of 2026. In its 2024 budget, the State Bar anticipated that its Admissions Fund would exhaust its reserves by 2026. In March 2024, the State Bar reported that it was exploring the use of a hybrid bar exam, beginning with the February 2025 bar exam, that would allow applicants the option to take the exam remotely and help the State Bar manage its costs. In October 2024, while the Supreme Court was also considering the Blue Ribbon Commission report, the State Bar petitioned the Supreme Court to allow it to administer the bar exam remotely. The State Bar’s primary motivation for this change was financial, however other considerations were also important drivers, including test-taker preference, access and cost-savings for applicants, as well as improved flexibility for both the State Bar and applicants.

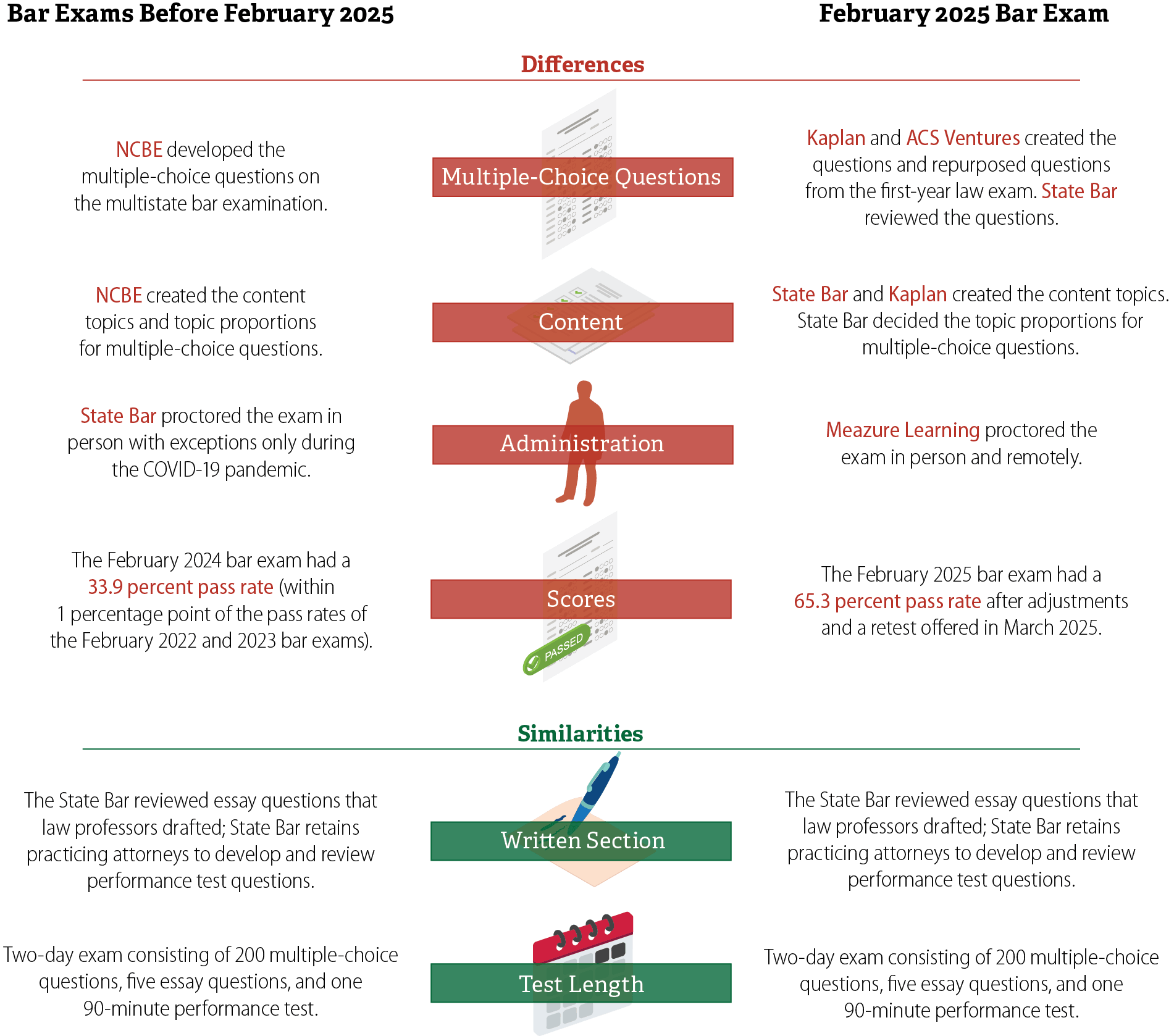

In August 2024, the State Bar contracted with Kaplan to develop multiple-choice questions for the February 2025 bar exam, and in November 2024, it contracted with Meazure Learning to provide exam administration services. In addition, the State Bar had an existing contract with ACS Ventures to provide psychometric consulting services and analysis. Psychometrics is the science of measuring psychological attributes, such as intelligence or understanding, and a psychometrician’s work ensures that tests are reliable and results are valid. The 2023 contract authorized ACS Ventures to provide additional research and advice services as requested by the State Bar, a clause which the State Bar used for ACS Ventures to help develop multiple-choice test questions to supplement the questions that Kaplan provided. The text box lists the contractors that the State Bar engaged to assist with the bar exam. We discuss all three contracts and the State Bar’s processes for developing and administering the February 2025 bar exam in greater detail in the sections that follow. Figure 2 shows similarities and differences between the February 2025 bar exam and prior bar exams, which had to comply with NCBE requirements.

Contractors the State Bar Engaged to Help Develop the Bar Exam

- Kaplan

- Develop multiple-choice questions for the bar exam.

- Meazure Learning

- Administer and proctor exams.

- ACS Ventures

- Psychometric services (exam validity and reliability testing) and analysis related to the bar exam.

- Additional research and advice services as requested by the State Bar.

Source: Kaplan, Meazure Learning, and ACS Ventures contracts.

Figure 2

The State Bar Made Changes to the February 2025 Bar Exam, Including in Exam Development, Administration, and Scoring

A graphic that shows differences in how the State Bar developed and administered the bar exam prior to February 2025, as well as similarities between prior bar exams and the February 2025 bar exam.

Differences

Multiple-Choice Questions

Before the February 2025 bar exam: The NCBE developed the multiple-choice questions on the multistate bar examination.

For the February 2025 bar exam: Kaplan and ACS Ventures created the questions and repurposed questions from the first-year law exam. State Bar reviewed the questions.

Content

Before the February 2025 bar exam: NCBE created the content topics and topic proportions for multiple-choice questions.

For the February 2025 bar exam: The State Bar and Kaplan created the content topics. State Bar decided the topic proportions for multiple-choice questions.

Administration

Before the February 2025 bar exam: The State Bar proctored the exam in person with exceptions only during the COVID-19 pandemic.

For the February 2025 bar exam: Meazure Learning proctored the exam in person and remotely.

Scores

Before the February 2025 bar exam: The February 2024 bar exam had a 33.9 percent pass rate (within 1 percentage point of the pass rates of the February 2022 and 2023 bar exams).

For the February 2025 bar exam: The February 2025 bar exam had a 65.3 percent pass rate after adjustments and a retest offered in March 2025.

Similarities

Written Section

The State Bar reviewed essay questions that law professors drafted; State Bar retains practicing attorneys to develop and review performance test questions.

Test Length

Two-day exam consisting of 200 multiple-choice questions, five essay questions, and one 90-minute performance test.

Source: State Bar website, NCBE website, and State Bar documentation on exam administration.

Contracting Requirements That Apply to the State Bar

The State Bar must follow the requirements for public contracting set forth in the State Bar Act and in rules the State Bar adopts. The State Bar Act requires the State Bar to comply with certain standards in the California Public Contract Code, such as competitive bidding requirements, when awarding a contract for more than $100,000 for information technology (IT) goods and services or for more than $50,000 for other goods and services. However, if the purpose of such a contract is for the development or administration of licensing or proficiency examinations, state law exempts it from competitive bidding requirements. The State Bar Act also requires the State Bar to establish a request‑for‑proposals procedure in accordance with those general standards. The State Bar has developed its own processes for awarding contracts for less than $100,000 for IT goods and services and less than $50,000 for other goods and services. The State Bar procurement manual defines these processes and specifies which State Bar contracts must follow them.

Audit Results

- The State Bar’s Timeline and Poor Planning Created Challenges With Question Development

- Question Issues Forced the State Bar to Remove More Questions From Scoring Than It Had Intended

- The State Bar Contracted With Meazure Learning Without Fully Verifying Its Ability to Effectively Administer the February 2025 Bar Exam

- The State Bar Fell Short of Preventing the Technical and Administrative Failures That Occurred in the February 2025 Bar Exam

- The State Bar Experienced No Cost Savings on the February 2025 Bar Exam and at Least $4 Million in Revenue Losses

The State Bar’s Timeline and Poor Planning Created Challenges With Question Development

Key Points

- Despite contracting delays, the State Bar of California (State Bar) committed to using its own questions on the February 2025 Bar Examination (February 2025 bar exam). As a result, it had just six months to develop and validate questions for the multiple‑choice section of the exam.

- Under the terms of its contract with Kaplan Exam Services, LLC (Kaplan), the State Bar had the ability to monitor the vendor’s development of multiple‑choice questions. However, when the State Bar identified a content gap in the questions, the State Bar believed Kaplan did not have adequate time to address it because of the State Bar’s rushed timeline.

- To address the content gap it discovered, the State Bar asked ACS Ventures, LLC (ACS Ventures) to develop multiple-choice questions, allowing the use of artificial intelligence (AI). State Bar staff did not inform the State Bar’s executive director, Committee of Bar Examiners (Committee), or Board of Trustees (Board) of the decision to use AI, and the State Bar did not have provisions in its contract with ACS Ventures to ensure the quality of the questions the vendor provided.

The State Bar’s Contract With Kaplan Did Not Provide Adequate Time for the Development of Effective Multiple-Choice Questions

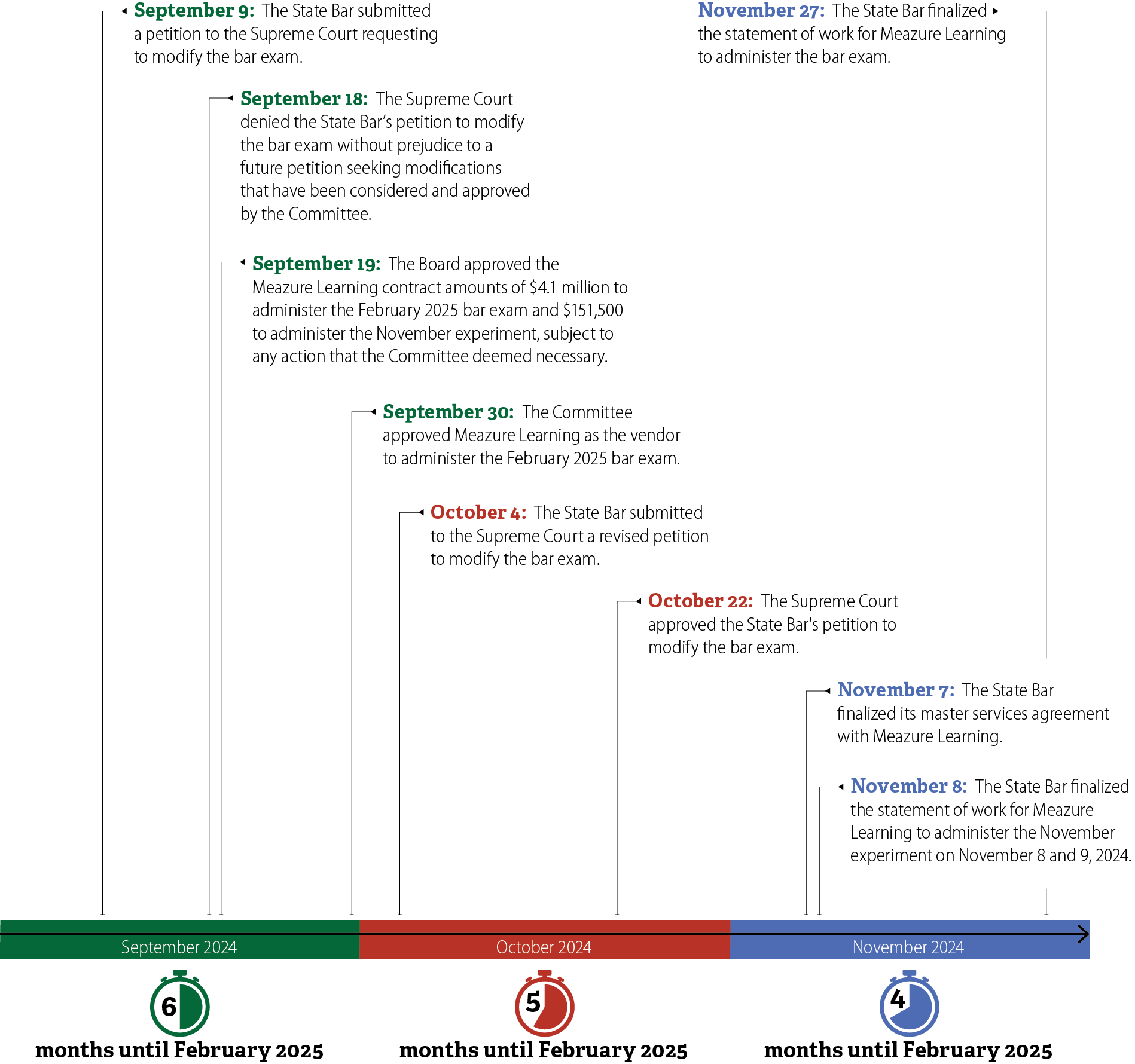

As we discuss in the Introduction, the State Bar could not offer the bar exam remotely if it continued to use multiple-choice questions from the National Conference of Bar Examiners (NCBE). According to an email from the State Bar’s former director of the Office of Admissions (admissions office) to Kaplan, the State Bar and Kaplan—the vendor with which the State Bar eventually contracted—discussed Kaplan’s ability to provide multiple-choice questions for the February 2025 bar exam as early as December 2023. In January 2024—13 months before the February 2025 bar exam—the State Bar issued a Request for Information (RFI) to identify other vendors that could develop multiple-choice questions modeled after the NCBE’s questions that covered the same legal topics.

The State Bar received Kaplan’s response to the RFI on February 9, 2024—more than a year before the February 2025 bar exam. Kaplan submitted the only valid response to the State Bar’s RFI, as the other interested vendor submitted its response three months after the RFI deadline. By May 2024, the State Bar was ready to present its proposed agreement with Kaplan to the Board. In its proposal, the State Bar included a general timeline showing that Kaplan would deliver questions starting in June 2024. However, two days before the May Board meeting, the NCBE sent Kaplan a letter stating that it sought to ensure that Kaplan would not use the NCBE’s copyrighted materials to create multiple-choice questions for California.4 On the day of the Board meeting, Kaplan requested the State Bar to defer the discussion of the proposed agreement because of the communication it received from NCBE, and the State Bar withdrew the item from the May 2024 agenda.

The State Bar and Kaplan continued to negotiate after the May 2024 Board meeting and introduced a shared cost provision into their contract, under which the State Bar would cover 50 percent of any potential litigation costs if the NCBE initiated any claims for copyright infringement. Although Kaplan would have preferred to develop questions for the July 2025 bar exam instead of the February exam to ensure its ability to meet or exceed expectations, it ultimately agreed to produce the questions for the February 2025 bar exam. In its July 2024 meeting, the Board authorized the executive director to execute a contract with Kaplan, which both parties signed on August 9, 2024. Instead of beginning question development in June 2024 as the State Bar planned, Kaplan was directed to deliver its first set of questions before September 2024.

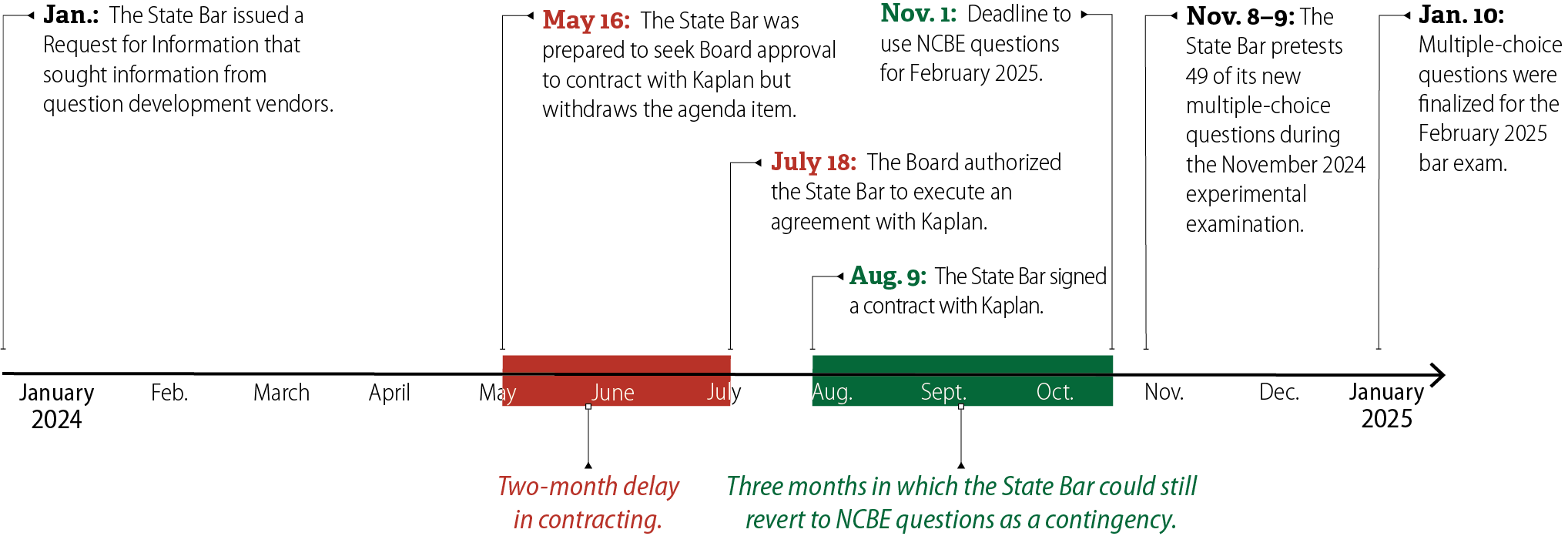

From signing the contract with Kaplan in August 2024 to administering the bar exam in February 2025, the State Bar had just six months to complete the entire process of developing and validating questions. In contrast, the NCBE may take up to three years to develop multiple-choice questions for the bar exam, a process that involves reviewing and editing questions multiple times. Further, the State Bar had just three months, from August 9 to November 1, to determine whether it would purchase the NCBE’s materials as a backup to Kaplan’s questions for the February 2025 exam, as Figure 3 shows. According to a letter the NCBE sent to the State Bar in May 2024, the admissions office had until November 1, 2024, to place its order for NCBE materials. After that date, the State Bar would not be able to revert to a contingency plan of returning to an in-person exam and using the NCBE questions for the February 2025 bar exam. Importantly, although the State Bar planned to pretest its questions in an experimental exam in October 2024, its shortened timeline meant that it could not conduct this experiment until November 8, after the deadline to decide to use NCBE questions had already passed.

Figure 3

The Delay in the State Bar’s Contracting With Kaplan Limited the State Bar’s Question Development Timeline

A timeline displaying an overview of State Bar’s procurement and exam development events, including a delay that halted the procurement process. These events are:

January 2024

The State Bar issued a Request for Information that sought information from question development vendors.

May 16

The State Bar was prepared to seek Board approval to contract with Kaplan but withdraws the agenda item. As a result, there is a two-month delay in contracting with Kaplan.

July 18

The Board authorized the State Bar to execute an agreement with Kaplan.

August 9

The State Bar signed a contract with Kaplan. This begins the three month period in which the State Bar could still revert to NCBE questions as a contingency.

November 1

Deadline to use NCBE questions for February 2025.

November 8-9

The State Bar pretests 49 of its new multiple-choice questions during the November 2024 experimental examination.

January 10, 2025

Multiple-choice questions were finalized for the February 2025 bar exam.

Source: State Bar Board meeting minutes, State Bar Board staff reports, the State Bar’s contract with Kaplan, and the NCBE’s letter to the State Bar.

At the time, the State Bar believed that it would be able to create and validate its new questions in time for the February exam despite the contracting delay. However, the current chief of the admissions office stated that, in hindsight, the timeline for question development was rushed and that the office did not allocate adequate time or resources to ensure the effectiveness of the February 2025 multiple-choice section of the bar exam. After the NCBE November 1 deadline, the State Bar agrees that it was committed to using its own questions on the February 2025 bar exam with no established alternative source for questions should problems arise.

The State Bar’s Contract With Kaplan Did Not Ensure That It Had Questions for All Required Exam Topics

The State Bar incorporated into its contract with Kaplan best practices from its procurement manual, some of which the text box lists. For example, the contract specified when Kaplan was required to deliver batches of questions and the number of questions in those batches. Additionally, the contract stated the State Bar’s intention to review Kaplan’s work product and provide it with prompt feedback, which it required Kaplan to address within 10 days. The chief of the admissions office said that Kaplan successfully delivered the required questions and met its contractual obligations.

Select Best Practices for Monitoring Vendor Performance

- Conduct status review of vendor compliance at regularly scheduled project meetings.

- Require written monthly or quarterly reviews of the vendor’s performance in meeting goals.

- Require the vendor to propose and implement plans to cure unsatisfactory performance when contract goals are not met.

Source: The State Bar Procurement Manual.

However, the State Bar did not specify in its contract with Kaplan the topics within each of the seven subjects that the State Bar needed for the February 2025 bar exam, which resulted in a shortage of questions in certain exam topics. The multiple-choice questions in each bar exam cover seven subjects and specific topics under each subject.5 Typically, the NCBE releases content outlines that inform test takers on the subjects, topics within subjects, and the proportions of questions allocated to each topic. While the State Bar and Kaplan could not use the NCBE’s resources due to copyright concerns, it also could not alter the bar exam in a way that would require a substantial modification of the training or preparation needed for passage without providing two years’ notice. According to the admissions office’s principal program analyst, the State Bar had to create its own content outlines with similar topics and proportions so test takers could prepare for the 2025 bar exam in the same manner as they would prepare for the exam if the State Bar used the NCBE’s multiple‑choice questions. The State Bar and Kaplan did not finalize its content outlines until late October 2024, over two months after the contract was signed. The State Bar’s contract required Kaplan to produce an approximately equal number of questions in each of the seven subjects but did not specify topics within the subjects, nor did it specify who would determine the proportions for different topics. The contract also allowed Kaplan to draft the questions using questions from the State Bar’s First-Year Law Students’ Exam (first-year exam) that the State Bar provided to Kaplan.6 The admissions office’s principal program analyst stated that the admissions office was not thinking of content proportions when selecting the first-year exam questions Kaplan could use, which the State Bar sent to Kaplan in September and October 2024

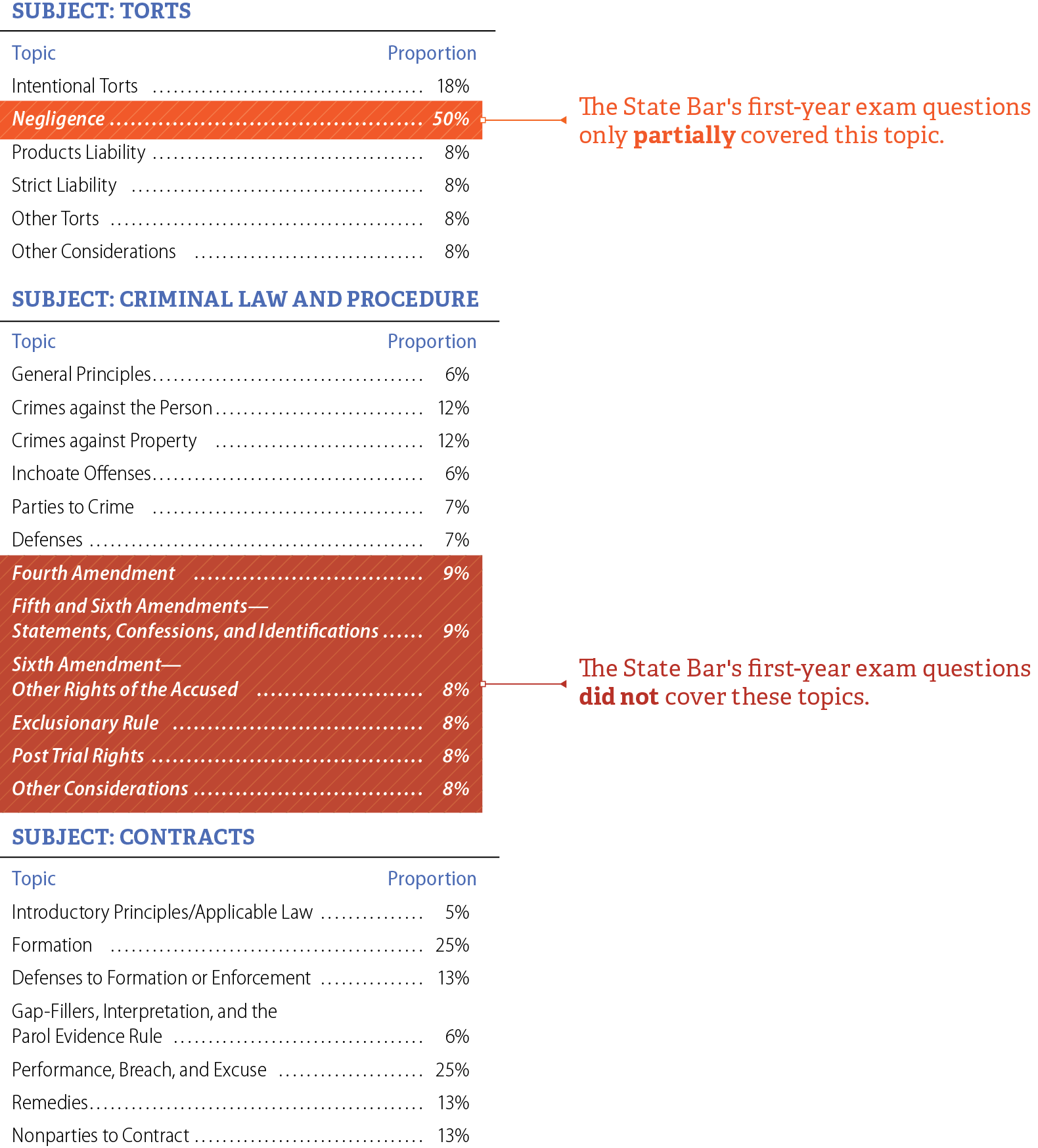

The State Bar’s late consideration of topics resulted in a content gap once it realized the first-year exam questions did not cover all the topics needed for the bar exam. The first‑year exam includes questions from three of the seven subjects on the bar exam. Because Kaplan was allowed to use the State Bar’s selected first-year exam questions, Kaplan did not produce questions in the subjects covered by the first-year exam. However, the first‑year exam does not fully cover all the topics within those subjects. As Figure 4 shows, by repurposing first-year exam questions, the State Bar did not ensure that questions were created to cover these topics, essentially creating a content gap in several topics. The admissions office did not identify the content gap until October 2024, when the State Bar began considering the question proportions for the February 2025 bar exam. According to the chief of the admissions office, the State Bar would have been more prepared to meet the content proportion requirements had the admissions office recognized and planned for the missing topics when contracting with Kaplan. Instead, the State Bar did not specify the topics in the contract, resulting in the State Bar needing additional questions to cover the overlooked topics.

Figure 4

The State Bar’s First-Year Exam Questions Did Not Fully Cover All Necessary Bar Exam Topics, Resulting in A Content Gap

A diagram listing the subjects that are tested on the first-year exam, the topics within those subjects, and the proportion of the subject allocated to each topic:

Torts

Intentional Torts, 18%

Negligence, 50%

Products Liability, 8%

Strict Liability, 8%

Other Torts, 8%

Other Considerations, 8%

Criminal Law

General Principles, 6%

Crimes against the Person, 12%

Crimes against Property, 12%

Inchoate Offenses, 6%

Parties to Crime, 7%

Defenses, 7%

Fourth Amendment, 9%

Fifth and Sixth Amendments—Statements, Confessions, and Identifications, 9%

Sixth Amendment—Other Rights of the Accused, 8%

Exclusionary Rule, 8%

Post Trial Rights, 8%

Other Considerations, 8%

Contracts

Introductory Principles/Applicable Law, 5%

Formation, 25%

Defenses to Formation or Enforcement, 13%

Gap-Fillers, Interpretation, and the Parol Evidence Rule, 6%

Performance, Breach, and Excuse, 25%

Remedies, 13%

Nonparties to Contract, 13%

The State Bar’s first-year exam questions only partially covered the topic of Negligence within the subject of Torts. The State Bar’s first-year exam questions did not cover the topics of Fourth Amendment, Fifth and Sixth Amendments-Statements, Confessions, and Identifications, Sixth Amendment-Other Rights of the Accused, Exclusionary Rule, Post Trial Rights, or Other Considerations. The State Bar’s first-year exam questions fully covered the topics within the subject of Contracts.

Source: State Bar February 2025 bar exam content outlines and question documentation.

The admissions office’s principal program analyst said that after the admissions office identified the need for additional questions, it assumed that Kaplan would be unable to produce the necessary questions or adjust the questions already in development because of time constraints. He added that the admissions office reached this conclusion because Kaplan was not obligated to create questions within subjects covered by the first-year exam and was already tasked with creating the February 2025 bar exam’s content outlines, which were outside the scope of their original work. Instead of determining how to extend its question development time frame, the admissions office’s staff asked ACS Ventures—the vendor that provided psychometric consulting services—to draft the additional questions.

By Allowing ACS Ventures to Use AI to Develop Exam Questions, the State Bar Increased the Risk of Performance Issues

The State Bar first discussed the possibility of using AI to produce bar exam questions in May 2024. At that time, the former director of the admissions office, special counsel of the admissions office, and ACS Ventures discussed the possibility of drafting questions using AI as a starting point, likely because Kaplan requested the State Bar defer the discussion of its proposal from the May 2024 Board meeting. However, in August 2024, the State Bar executed its contract with Kaplan to develop multiple‑choice questions for the February 2025 bar exam, seemingly rendering the need to use AI moot.

However, a month later in late September 2024, the State Bar asked ACS Ventures to develop multiple-choice questions after realizing it did not have an adequate number of questions from Kaplan for the November 2024 Experimental Examination (November experiment).7 The State Bar planned the November experiment to pretest a sample of its new multiple-choice questions. Its contract required Kaplan to deliver 35 questions to the State Bar no later than September 25, 2024, so the State Bar would have sufficient time to validate their quality before testing those questions during the November experiment. However, two days before the State Bar executed its contract with Kaplan in August 2024, ACS Ventures recommended that the State Bar instead test 49 questions during the November experiment. Although the State Bar accepted ACS Ventures’ recommendation, it did not amend its contract with Kaplan to include the additional questions, resulting in a shortage of 14 questions for the November experiment.

The admissions office’s principal program analyst believed that Kaplan could not have developed more questions for the November experiment because Kaplan was already operating under tight deadlines—Figure 5 shows how the condensed content development time frame limited flexibility to address the content shortage. Consequently, the admissions office asked ACS Ventures to develop the missing 14 questions. ACS Ventures drafted 14 questions for the November experiment using AI. Of those questions, the State Bar reports that it chose to carry over 11 that were well-performing to use on the February 2025 bar exam.

Figure 5

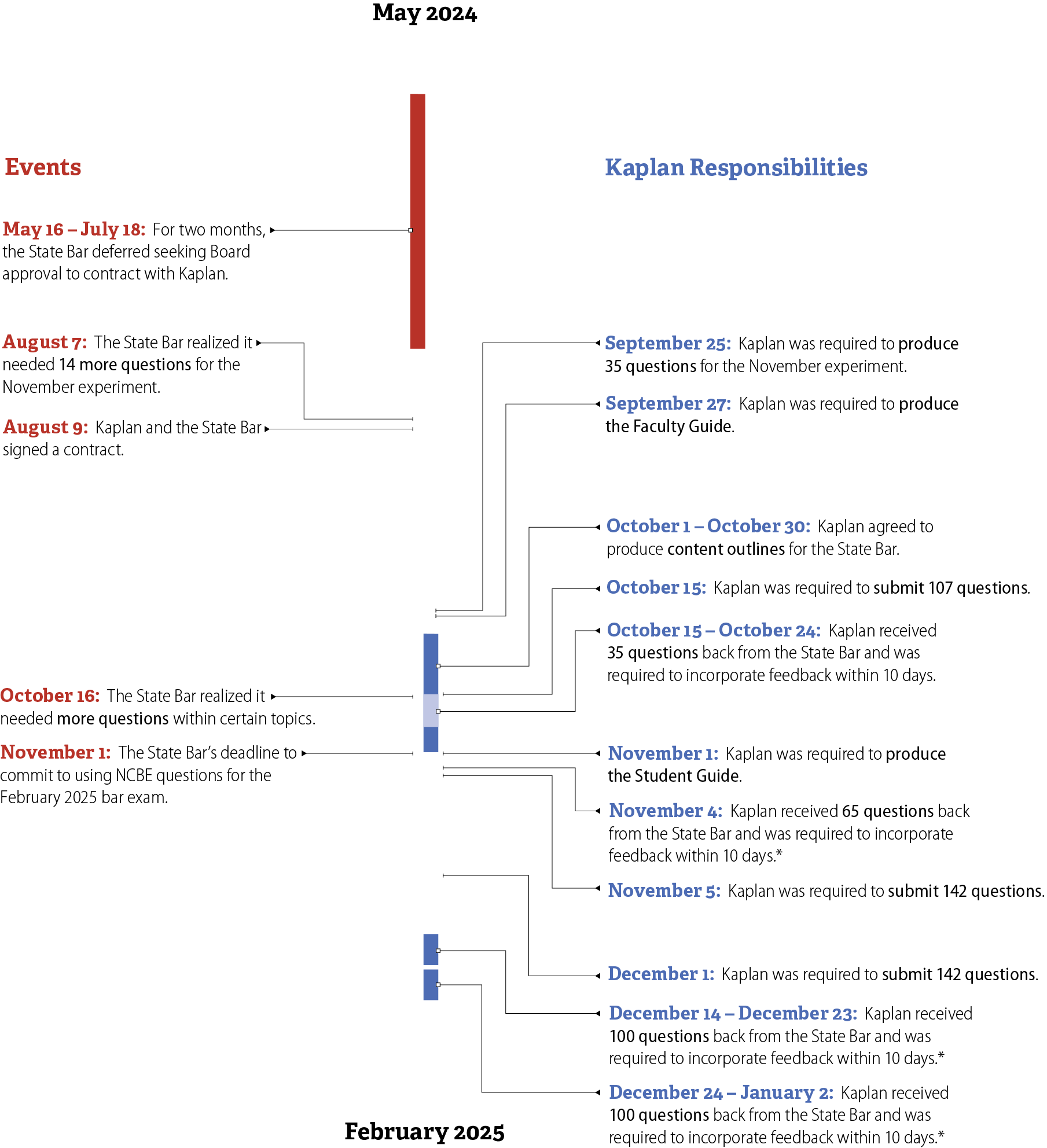

The State Bar’s Condensed Content Development Time Frame Left the State Bar and Kaplan With Limited Flexibility to Address Question Deficiencies

A timeline that outlines the State Bar’s and Kaplan’s question development process from the contracting delay in May 2024 to February 2025. The timeline is split into two categories: events and Kaplan’s responsibilities.

Events

May 16-July 18: For two months, the State Bar deferred seeking Board approval to contract with Kaplan.

August 7: The State Bar realized it needed 14 more questions for the November experiment.

August 9: Kaplan and the State Bar signed a contract.

October 16: The State Bar realized it needed more questions within certain topics.

November 1: The Stater Bar’s deadline to commit to using NCBE questions for the February 2025 bar exam.

Kaplan Responsibilities

September 25: Kaplan was required to produce 35 questions for the November experiment.

September 27: Kaplan was required to produce the Faculty Guide.

October 1-October 30: Kaplan agreed to produce content outlines for the State Bar.

October 15: Kaplan was required to submit 107 questions.

October 15-October 24: Kaplan received 35 questions back from the State Bar and was required to incorporate feedback within 10 days.

November 1: Kaplan was required to produce the Student Guide.

November 4: Kaplan received 65 questions back from the State Bar and was required to incorporate feedback within 10 days. Kaplan only reviewed questions that were Kaplan-developed. The State Bar did not send first-year questions back to Kaplan.

November 5: Kaplan was required to submit 142 questions.

December 1: Kaplan was required to submit 142 questions.

December 14-December 23: Kaplan received 100 questions back from the State Bar and was required to incorporate feedback within 10 days. Kaplan only reviewed questions that were Kaplan-developed. The State Bar did not send first-year questions back to Kaplan.

December 24-January 2: Kaplan received 100 questions back from the State Bar and was required to incorporate feedback within 10 days. Kaplan only reviewed questions that were Kaplan-developed. The State Bar did not send first-year questions back to Kaplan.

The timeline shows how Kaplan had a short period of time to meet many deliverables between September 2024 and January 2025, which was further complicated by the need for more questions and the NCBE’s deadline.

Source: State Bar internal item tracking sheet, emails, Kaplan contract, and State Bar staff.

* Kaplan only reviewed questions that were Kaplan developed. The State Bar did not send first-year exam questions back to Kaplan.

Thus, when the State Bar identified a content shortage in the questions that Kaplan was developing for the February 2025 bar exam, it once again contacted ACS Ventures. Specifically, the former program director in the admissions office sent an email to ACS Ventures asking it to produce the additional questions. As Figure 6 illustrates, the State Bar ultimately included on the February 2025 bar exam 29 questions that ACS Ventures developed using open-source generative AI. We discuss the content and quality of these questions in a subsequent section.

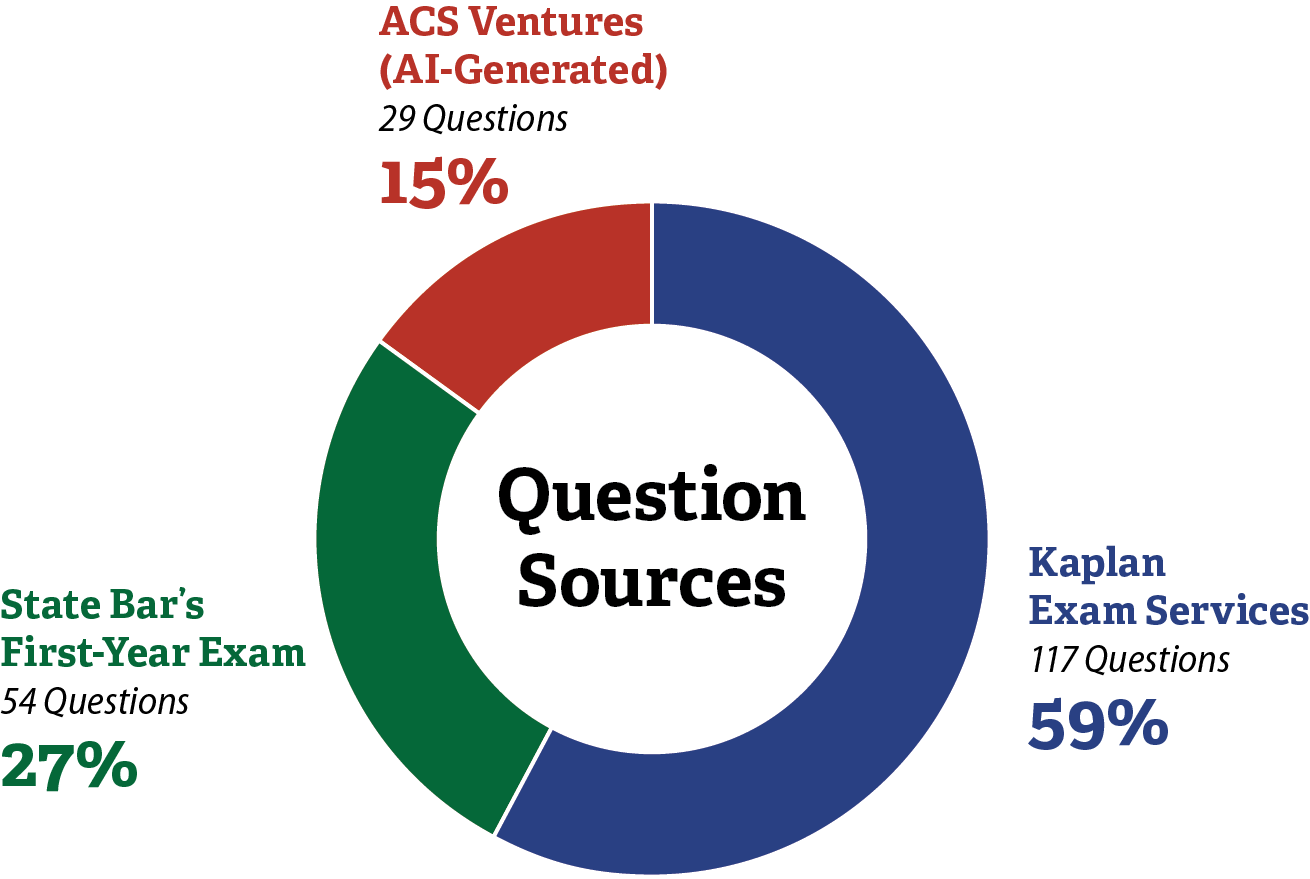

Figure 6

Kaplan Did Not Develop All 200 Multiple-Choice Questions on the February 2025 Bar Exam

A pie chart showing the percentage out of 200 total questions, that ACS Ventures, Kaplan, and the State Bar each provided for the February 2025 bar exam. The figure also shows the count of questions from each source.

Kaplan Exam Services

Kaplan developed 59 percent of the multiple-choice questions, or 117 questions, on the February 2025 bar exam.

State Bar’s First-Year Exam

27 percent of the multiple-choice questions, or 54 questions, were repurposed first-year exam questions.

ACS Ventures (AI-Generated)

ACS Ventures created 15 percent of the multiple-choice questions, or 29 questions, using AI.

The percentages do not add up to 100 due to rounding.

Source: State Bar master bar exam question tracking spreadsheet.

Note: Percentages do not add up to 100 due to rounding.

The State Bar did not amend its contract with ACS Ventures to account for the creation of test questions or establish safeguards before directing the vendor to draft questions for the February 2025 bar exam. Although the State Bar included provisions associated with the use of AI in Kaplan’s contract, as the text box shows, the State Bar’s contract with ACS Ventures did not have similar provisions. It executed its contract with ACS Ventures in December 2023 for psychometric services and analysis related to the bar exam and first-year exam and amended it in November 2024 to increase compensation for services. The contracts did not account for the creation of exam question development but included a provision allowing for ACS Ventures to provide other advice services as the State Bar requested. Prior to amending the contract—in September and October 2024—the State Bar asked ACS Ventures to develop questions for the November experiment and for the February 2025 bar exam. Neither the 2023 contract nor its amendment covered the services provided to the State Bar related to question development or ACS Ventures’ use of AI. The State Bar’s procurement manual and the office of general counsel’s contract procedures do not address how staff should use contract provisions that allow for additional services. This lack of guidance limits oversight and increases the risk that State Bar staff will direct contractors to perform services without clearly defining expectations or controls.

The State Bar Included the Following Requirements Related to the Use of AI in its Contract with Kaplan:

- Any use of AI must conform to the U.S. Copyright Office Guidance regarding the requirements for copyrightability and ownership.

- Humans shall conceive, execute, and actually form the elements of authorship in any work products, test materials, and individual test items, and any use of AI tools shall be solely to enhance elements of existing human-created work product.

- Kaplan shall disclose the extent and nature of its use of AI in connection with the creation of any work product prior to delivery.

Source: The State Bar’s contract with Kaplan.

The use of AI to develop questions was not inherently problematic. In fact, in October 2024, the Supreme Court issued an administrative order recommending that the State Bar review the availability of new technologies, such as AI, that could improve the reliability and cost‑effectiveness of testing. This direction indicates that the State Bar was able to pursue innovation in exam development. However, it did not implement this change through a transparent, structured process or clearly communicate its decisions to its former executive director and governing bodies, limiting oversight of a significant change to the examination approach.

The admissions office did not escalate the decision directing ACS Ventures to develop exam questions or the decision to allow the use of AI in that process. According to the admissions office’s principal program analyst, nobody currently at the State Bar can identify who made the decision to ask ACS Ventures to generate multiple-choice questions for use on the November experiment or the February 2025 bar exam. However, a former program director in the admissions office sent an email to ACS Ventures on October 30, 2024, asking it to assist with producing multiple-choice questions for use on the February 2025 bar exam. Although the former director of the admissions office was included on that email, and she and the special counsel of the admissions office had discussed the use of AI with ACS Ventures, neither they nor the State Bar’s staff informed the former executive director, the Committee, or the Board of the decision to use ACS Ventures to develop exam questions or that those questions would be generated using AI. The chief of the admissions office stated that, prior to the February 2025 bar exam, the State Bar did not have a documented framework requiring staff to escalate substantive changes to exam development methodology to executive leadership, including the former executive director and other members of the State Bar’s leadership team, or to governance bodies. The State Bar still lacks a policy that defines substantive changes and requires staff to escalate decisions on them to executive leadership. However, the State Bar is working to develop a framework it says will ultimately address this issue by July 2026.

Ultimately, the State Bar allowed ACS Ventures to perform multiple roles across exam development, validation, and post-exam performance analysis, as Figure 7 illustrates. By assigning these responsibilities to a single vendor, the State Bar created the appearance that ACS Ventures influenced question development, evaluation, and scoring. The State Bar acknowledged that this concentration of responsibilities increased the risk of perceived conflicts of interest in the exam development process.

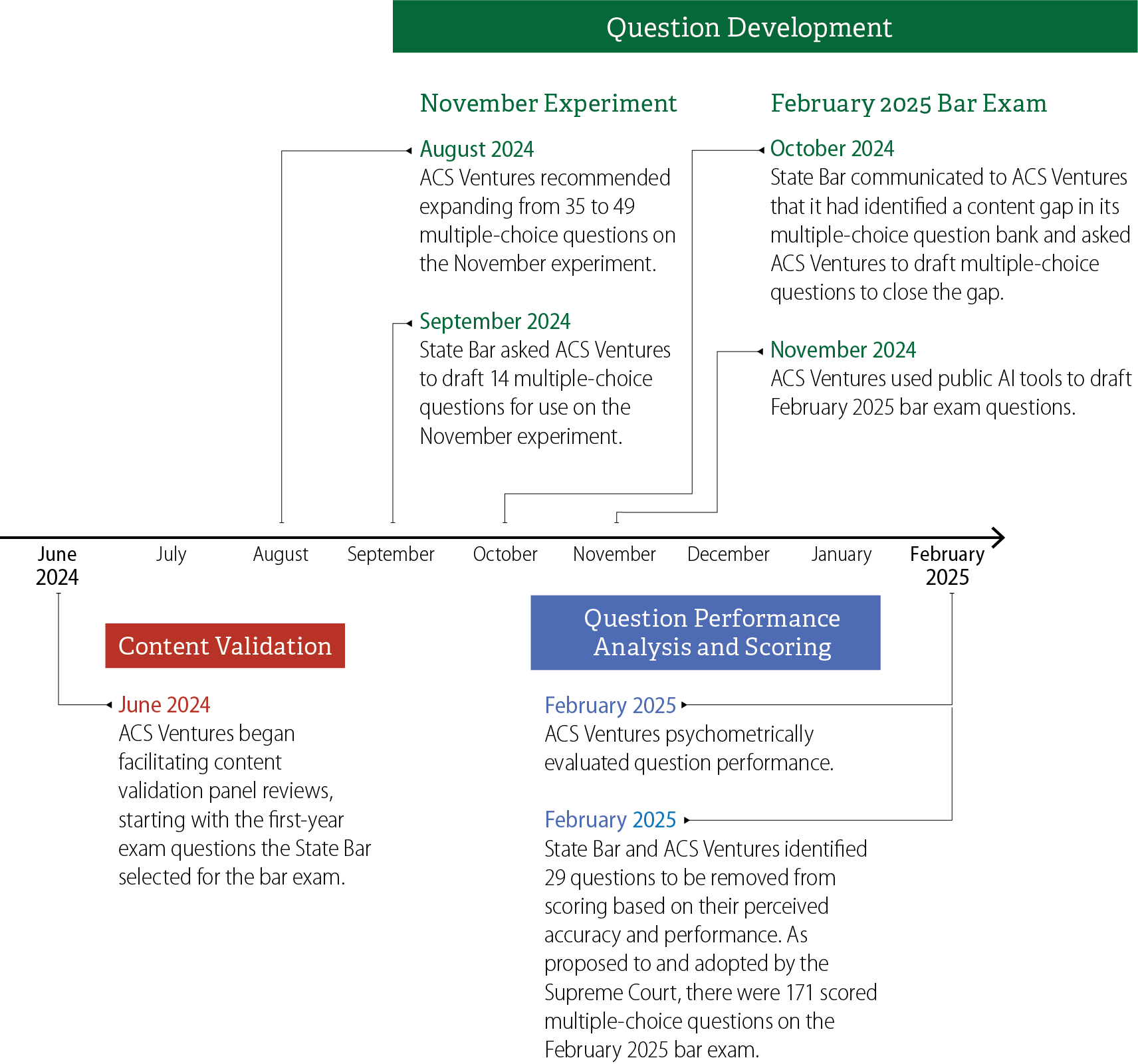

Figure 7

ACS Ventures Involvement in Multiple Stages of the Development and Assessment of the February 2025 Bar Exam Increased the Risk of Perceived Conflicts of Interest

A timeline from June 2024, when the first content validation panel review session occurred, to the post-exam analysis period in February 2025. The timeline highlights ACS Venture’s multiple roles during content validation, question development, and question performance analysis and scoring.

Content Validation

June 2024: ACS Ventures began facilitating content validation panel reviews, starting with the first-year exam questions the State Bar selected for the bar exam.

Question Development

November Experiment

August 2024: ACS Ventures recommended expanding from 35 to 49 multiple-choice questions on the November experiment.

September 2024: State Bar asked ACS Ventures to draft 14 multiple-choice questions for use on the November experiment.

February 2025 Bar Exam

October 2024: State Bar communicated to ACS Ventures that it had identified a content gap in its multiple-choice question bank and asked ACS Ventures to draft multiple-choice questions to close the gap.

November 2024: ACS Ventures used public AI tools to draft February 2025 bar exam questions.

Question Performance

February 2025: ACS Ventures psychometrically evaluated question performance.

February 2025: State Bar and ACS Ventures identified 29 questions to be removed from scoring based on their perceived accuracy and performance. As proposed to and adopted by the Supreme Court, there were 171 scored multiple-choice questions on the February 2025 bar exam.

Source: State Bar documentation, correspondence records, staff confirmations, and the State Bar’s April 2025 petition to the Supreme Court related to scoring adjustments.

Question Issues Forced the State Bar to Remove More Questions From Scoring Than It Had Intended

Key Points

- The State Bar used content validation panels and subject matter expert reviews to ensure that the multiple-choice questions were appropriate for the February 2025 bar exam. However, its implementation of each of these processes had significant weaknesses.

- Following the February 2025 bar exam, ACS Ventures identified that 40 of the 200 multiple-choice questions on the exam had performance issues. While the State Bar intended to remove 25 questions from scoring, it ultimately did not include 29 questions in the test takers’ scores.

The State Bar Did Not Adequately Ensure the Quality of the Multiple-Choice Questions It Included in the February 2025 Bar Exam

The State Bar primarily used three processes to ensure the quality of the multiple-choice questions it used on the February 2025 bar exam: content validation panel review, subject matter expert review, and pretesting. However, the State Bar’s execution of its content validation process had flaws that significantly hindered its effectiveness. First, when the State Bar recruited its content validation panels, it did not follow industry standards for selecting panelists. Second, the State Bar assigned only one subject matter expert and did not ensure that the subject matter expert reviewed all questions. Third, the State Bar lacked enough time to pretest most of its new multiple-choice questions before the February 2025 bar exam. Consequently, the State Bar either did not identify or did not have time to address all problematic questions before administering the exam.

Content Validation Panels

As Figure 8 shows, the State Bar engaged in a content validation process to review and edit the newly developed multiple-choice questions for administration on the February 2025 bar exam. According to the chief of the admissions office, the State Bar relied on ACS Ventures to create that process to validate the appropriateness of questions for use on the February 2025 bar exam. In the process’s first step, ACS Ventures facilitated multiple content validation panels composed primarily of law school faculty and recently licensed attorneys (legal professionals). The admissions office selected the content validation panelists and under the facilitation of ACS Ventures, these panels used the evaluation criteria the text box presents to review the multiple-choice questions over several nonconsecutive days. The State Bar’s legal professionals reviewed all multiple-choice questions without knowing their source.

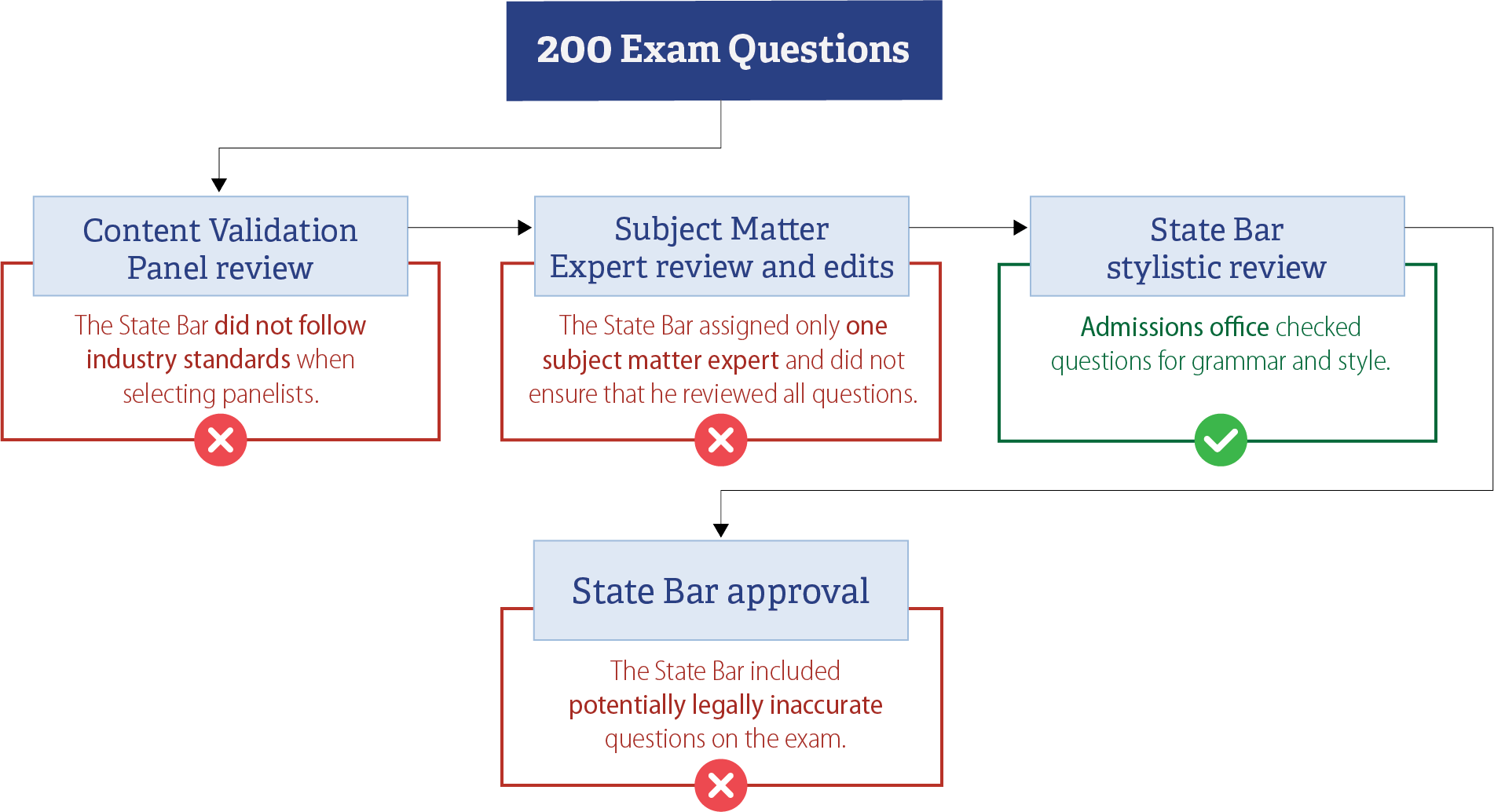

Figure 8

The State Bar’s Execution of Its Content Validation Process Had Weaknesses in Multiple Stages

A flow chart listing the steps in the State Bar’s content validation process and, for each step, any weaknesses in the State Bar’s execution of the process. The 200 February 2025 bar exam questions went through the following steps during the content validation process:

1. Content Validation Panel review

The State Bar did not follow industry standards when selecting panelists.

2. Subject Matter Expert review and edits

The State Bar assigned only one subject matter expert and did not ensure that he reviewed all questions.

3. State Bar stylistic review

Admissions office checked questions for grammar and style. We did not identify weaknesses in this step.

4. State Bar approval

The State Bar included potentially legally inaccurate questions on the exam.

Note: The State Bar sent questions that Kaplan developed back to Kaplan, which adjusted the questions based on the feedback and returned the questions to the State Bar, and subsequently sent the questions back to the subject matter expert for another review.

Source: State Bar master bar exam question tracking spreadsheet.

Note: The State Bar sent questions that Kaplan developed back to Kaplan, which adjusted the questions based on the feedback and returned the questions to the State Bar, and subsequently sent the questions back to the subject matter expert for another review.

Content Validation Panel Criteria

- Appropriateness of the topic area to which the item was originally classified.

- The technical accuracy of the item (i.e., the factual scenario and answer are correct, and distractors are plausible and wrong).

- The appropriateness of the item to provide evidence of minimal competency for an entry-level lawyer.

- The item content being free of any bias issues that could advantage or disadvantage diverse applicants.

Source: ACS Ventures’ Content Validation Panel Summary Report.

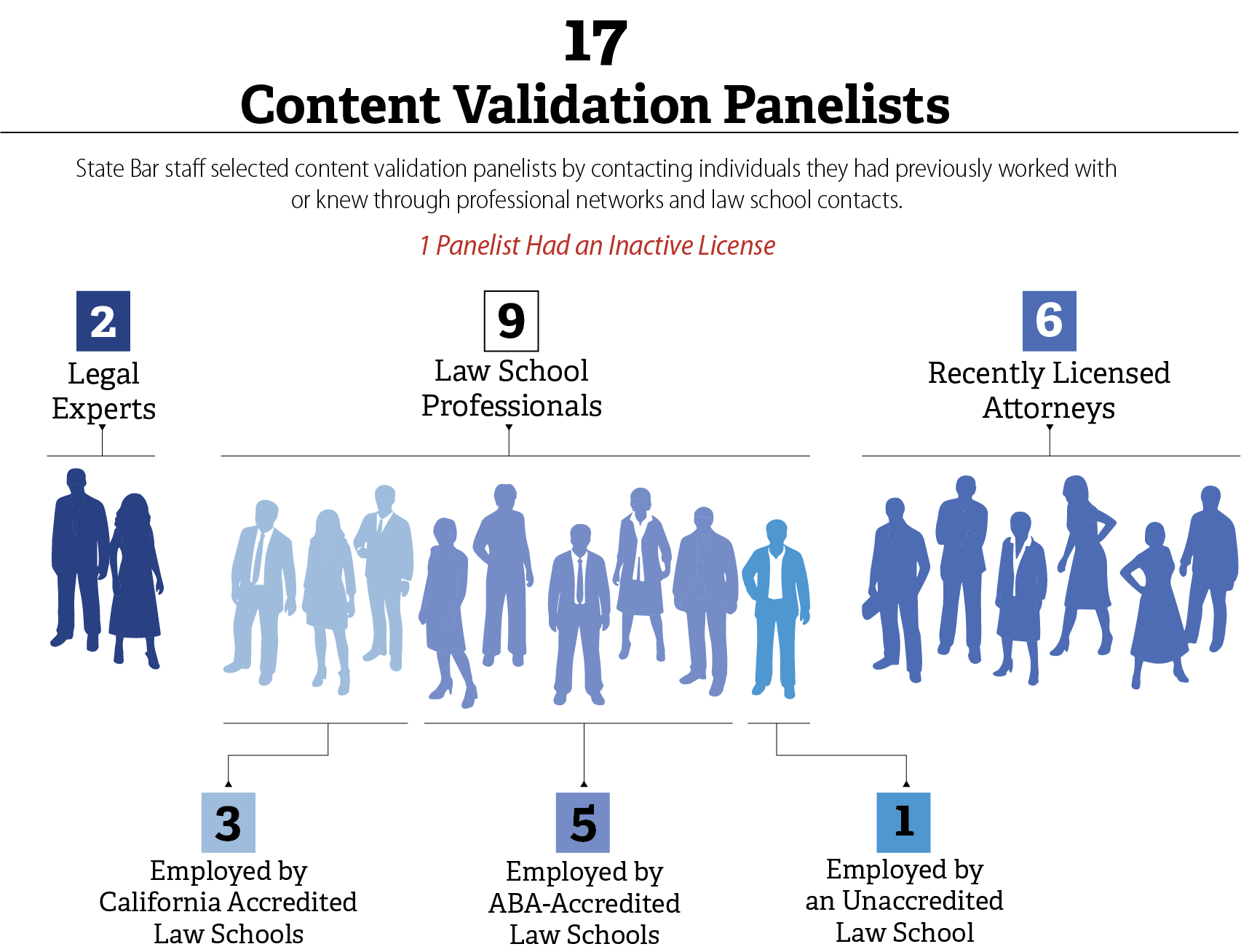

However, the State Bar did not follow established industry standards for selecting content validation panelists. The American Educational Research Association, the American Psychological Association, and the National Council on Measurement in Education provide criteria for the development and evaluation of educational and psychological testing. These standards state that a validation process that relies in part on the opinions or decisions of experts must establish procedures for selecting such experts, including their qualifications and experience. Consequently, the standards recommend that an organization should describe the basis for identifying certain groups of individuals as appropriate experts and document the procedures it uses to select those experts. Nonetheless, according to the admissions office’s principal program analyst, the State Bar did not document eligibility requirements for its panelists nor its process for recruiting and selecting its panelists.8 Instead, the admissions office states that it initially selected panelists by contacting individuals they had previously worked with or knew through professional networks and law school contacts and then later began identifying candidates by pulling reports of licensees who had been licensed within the previous five years.

The State Bar did not establish or document minimum qualification criteria or selection procedures for content validation panelists, contrary to testing standards. As a result, the State Bar could not ensure that panelists were selected based on defined expertise or consistent qualifications. Instead, panel composition reflected an inconsistent and informally derived mix of credentials, as Figure 9 illustrates. The former admissions office’s program director acknowledged that the State Bar did not conduct background checks on panelists based on the assumption that the panelists’ employers would already have conducted background checks. The admissions office’s principal program analyst confirmed that neither the Committee nor the Board oversaw the content validation panel recruitment or selection process conducted by admissions office’s staff. Consequently, the State Bar lacked assurance that its panels collectively possessed the qualifications necessary to support reliable and defensible content validation results. At the end of 2025, the Supreme Court approved policies that establish requirements for the eligibility, recruitment, and selection of content validation panelists and address deficiencies in the State Bar’s vetting process.

Figure 9

The State Bar Selected Content Validation Panelists With an Inconsistent Range of Credentials

A diagram grouping the 17 content validation panelists by their credentials to show how the State Bar recruited inconsistently across different legal professional categories. State Bar staff selected content validation panelists by contacting individuals they had previously worked with or knew through professional networks and law school contacts.

One panelist had an inactive license.

Two panelists were legal experts.

Nine panelists were law school professionals.

Six panelists were recently licensed attorneys.

Three panelists were employed by California Accredited Law Schools.

Five panelists were employed by ABA-Accredited Law Schools.

One panelist was employed by an Unaccredited Law School.

Note: Law schools approved by the American Bar Association (ABA-accredited) are nationally recognized by all bar admitting jurisdictions.

Source: State Bar documentation.

Note: Law schools approved by the American Bar Association (ABA-accredited) are nationally recognized by all bar admitting jurisdictions.

Seeking to improve the State Bar’s content validation panel selection process, the Committee adopted a policy in June 2025 that describes the eligibility, recruitment, and selection of content validation panelists. Specifically, the policy states that panelists must have held a license to practice law in at least one state and be in good standing in any state in which they are licensed. They must provide evidence that they have expertise in the knowledge and skills that will be tested and familiarity with the abilities required of an entry-level attorney. In determining whether panelists are well-qualified, the State Bar evaluates factors such as legal practice experience and subject matter expertise. The policy also directs the State Bar to use a broad solicitation process to recruit panelists and to limit recruitment of faculty to those employed by schools approved by the American Bar Association, California Accredited Law Schools (CALS), or law schools registered with the Committee. The Supreme Court approved this policy in December 2025.

Subject Matter Expert Review

As we describe previously, the purpose of the content validation panel review is to ensure that questions are appropriate—that is, that the questions test the correct topics and are free from bias. The NCBE engages in a similar process, in which committees composed of legal experts jointly determine the questions’ appropriateness. As an additional, independent check for bias and legal accuracy, the NCBE also employs two independent subject matter experts per subject, for a total of 14 subject matter experts who specialize in the subject areas of the questions they review.

In contrast to NCBE’s approach, the State Bar employed just one general subject matter expert to review all 200 of its multiple-choice questions before the February 2025 bar exam. While the State Bar’s content validation panels provided only recommendations, the State Bar’s subject matter expert edited the questions according to the instructions in the text box; the State Bar also encouraged the subject matter expert to identify disagreements he had with the panels’ recommendations. By employing only one subject matter expert, the State Bar limited the depth of that expert’s legal review and placed significant time pressure on him to correct issues before the exam, as he had to review eight batches of questions during the question development period. The admissions office’s program analyst could not explain why the State Bar assigned only one subject matter expert to review questions. To address this weakness, at a meeting in June 2025, the Committee approved a plan to recruit 21 subject matter experts—three subject matter experts for each exam subject—for future exam question validation processes.

The Subject Matter Expert Was Responsible for the Following:

- Ensuring that the question is keyed correctly.

- Ensuring that the topic or issue tested is correct.

- Editing questions so they follow the State Bar’s general multiple-choice question guidelines.

- Adding any additional comments or notes.

Source: The State Bar’s multiple-choice question review instructions.

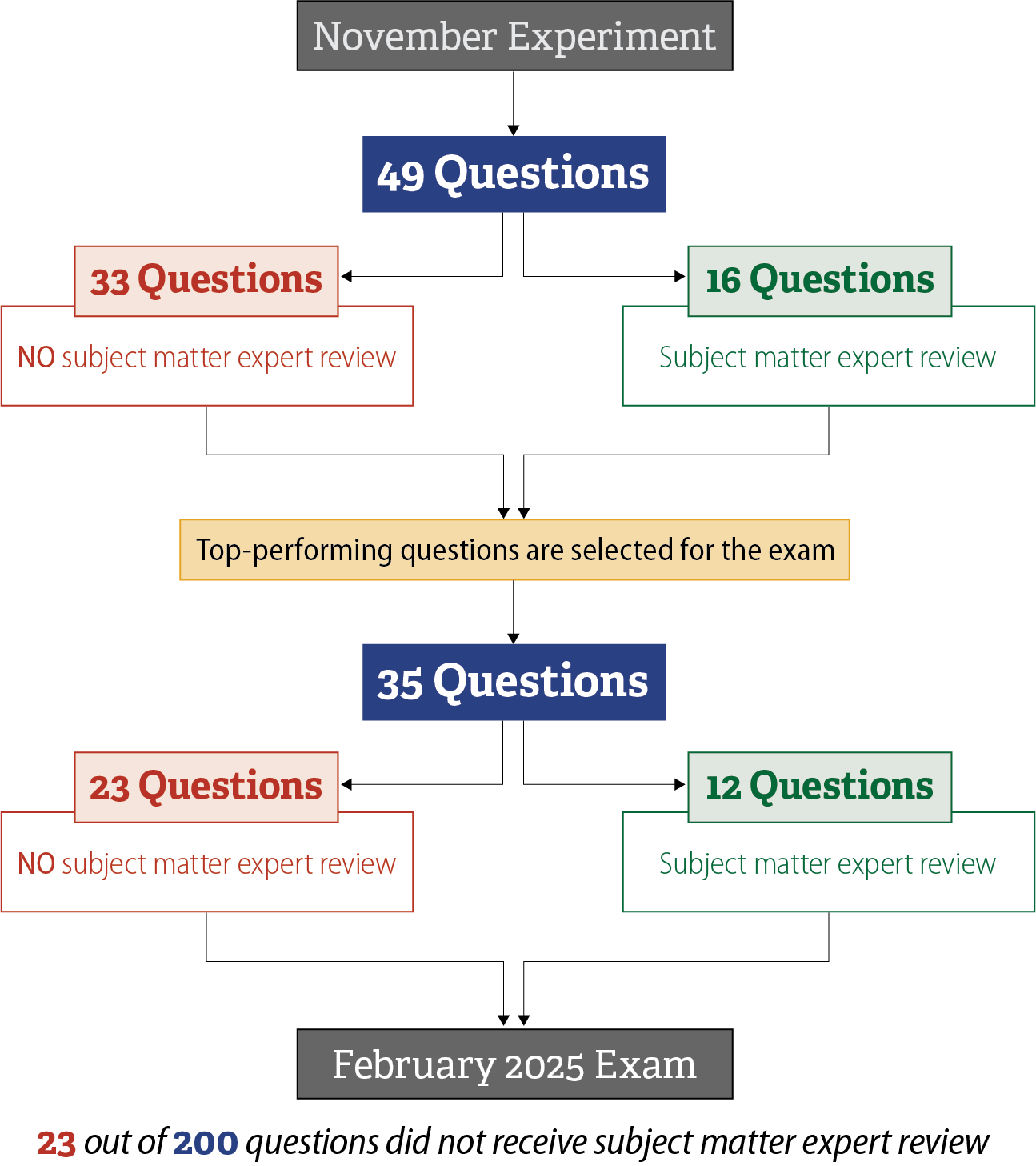

The State Bar also allowed 23 exam questions that had not been reviewed by its subject matter expert to appear on the February 2025 bar exam. As Figure 10 shows, the questions were originally among those in the November experiment. The subject matter expert did not review them because the State Bar did not believe it had time for such a review. The questions were the top-performing November experiment questions on the February 2025 bar exam and were used as benchmarks to measure the remaining questions’ performance. According to the chief of the admissions office, the State Bar did not review or edit these 23 questions before placing them on the February 2025 bar exam because it wanted to preserve the questions’ performance data. The State Bar later did not score four of the 23 questions, including two questions that the subject matter expert had identified as being potentially legally inaccurate, despite them being top-performing questions on the November experiment.

Figure 10

The State Bar Did Not Ensure That All February 2025 Bar Exam Questions Were Reviewed by Its Subject Matter Expert

A flow chart showing how the subject matter expert did not review 33 of the questions tested on the November experiment, eventually resulting in 23 February 2025 bar exam questions not receiving subject matter expert review.

Initially, 49 questions were tested on the November experiment. Out of the 49 questions, 33 of the November experiment questions did not receive subject matter expert review, while the remaining 16 did. The 35 top performing questions from the November experiment were selected for the February 2025 bar exam, of which 23 questions did not receive subject matter expert review while the other 12 did. As a result, 23 out of 200 February 2025 bar exam questions did not receive subject matter expert review.

Source: State Bar master bar exam question tracking spreadsheet.

The State Bar knew that, because of time constraints, the subject matter expert was unable to correct all identified problems and errors before it finalized the 200 questions that appeared on the February 2025 bar exam. Twelve days before the February 2025 bar exam, the State Bar tasked its subject matter expert with completing a final review of all 200 exam questions. The subject matter expert determined that 60 questions needed minor wording and grammar corrections and that six additional questions had potential legal inaccuracies. However, the State Bar did not incorporate these corrections or revisions because, according to the admissions office’s principal program analyst, it had already printed exam materials and uploaded the questions to the ProctorU Inc., dba Meazure Learning (Meazure Learning) platform. In its post‑exam psychometric analysis, the State Bar chose to remove the six potentially legally flawed questions from scoring.

Pretesting

The State Bar did not pretest all of the questions for the February 2025 bar exam, contrary to NCBE’s standard practice. According to the NCBE, pretesting is the process of presenting test takers with questions on the bar exam that will not be scored to ensure their effectiveness before they are used as scored questions on a future exam. Pretesting questions allows the NCBE to determine whether those questions demonstrate acceptable statistical characteristics; for example, a question must show evidence that test takers who answered it correctly also tended to obtain high scores on the entire exam. The NCBE’s standard practice is to pretest all multiple‑choice questions. Typically, the NCBE pretests its questions by including 25 of them as unscored questions on its bar exams, alongside 175 scored questions that have already been pretested.

Because the State Bar was developing a completely new exam, it did not have the ability to employ the NCBE’s method for pretesting questions before including them on the February 2025 bar exam. However, the admissions office’s program manager stated that during a Committee meeting stakeholders expressed their desire for the State Bar to pretest questions before they appeared on the February 2025 bar exam. As we described previously, the State Bar tested 49 of its exam questions by including them in the November experiment. The admissions office’s principal program analyst confirmed that the State Bar then used the 35 best‑performing November experiment questions on the February 2025 exam. Ultimately, the State Bar did not pretest the remaining 165 questions before including them on the bar exam. As a result, the State Bar did not have assurance that most of its questions had acceptable statistical characteristics before including them in the exam.

On the February 2025 Bar Exam, 40 of the 200 Multiple-Choice Questions Had Performance Issues and Six Raised Legal Accuracy Concerns

Because it was using new questions, the State Bar relied on post-exam statistical analysis to determine which of the February 2025 bar exam’s multiple-choice questions would count toward test takers’ scores. The State Bar intended to adopt a similar approach to the NCBE and score only 175 of the 200 questions. Unlike the NCBE’s practice of pretesting all exam questions before they are scored on the bar exam, the State Bar had not tested most of the 200 questions on the February 2025 bar exam. As such, the State Bar did not identify the questions it would remove from scoring until after ACS Ventures conducted psychometric analysis on all the questions.

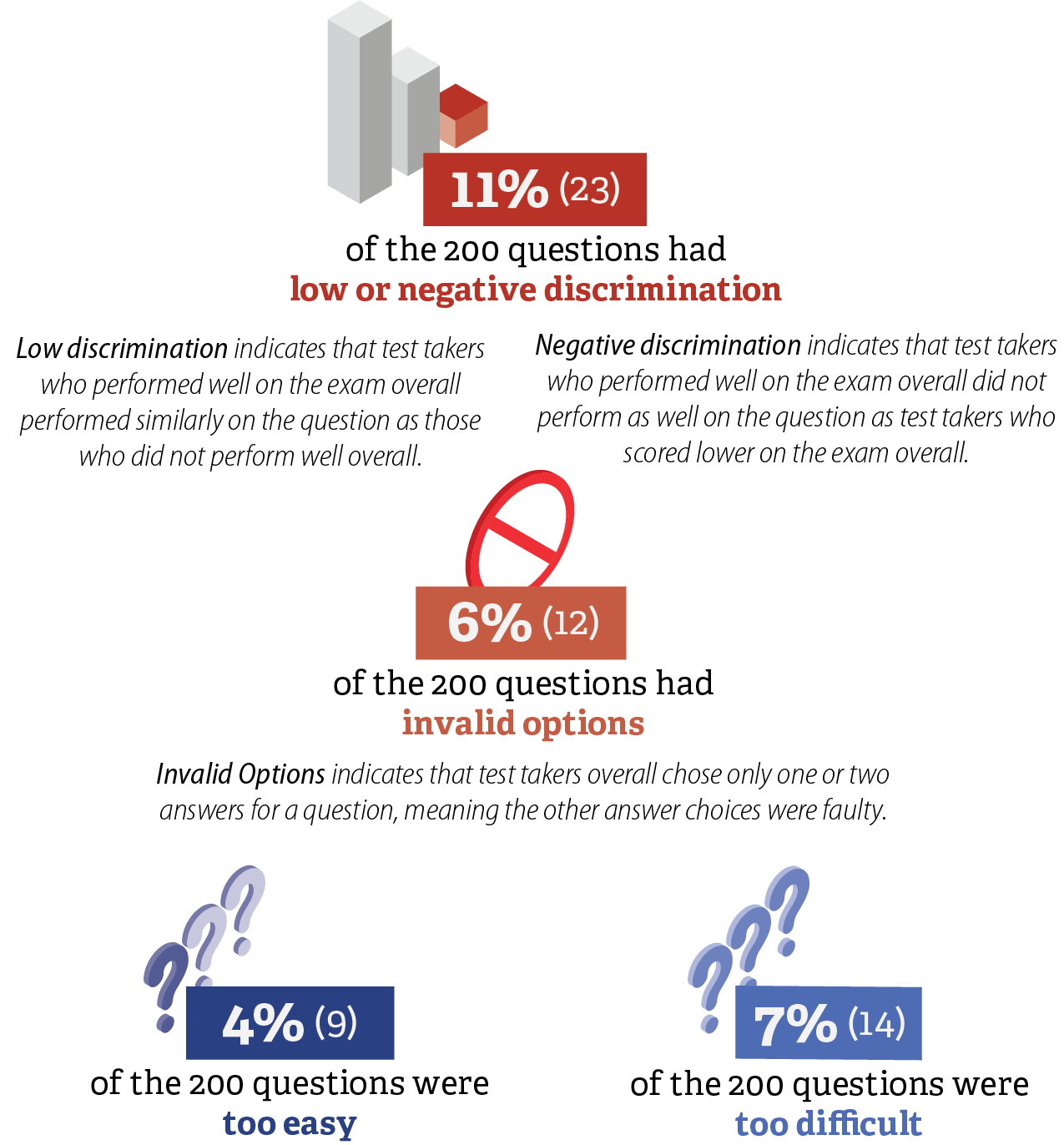

While the content validation process was a qualitative review of the questions’ legal accuracy before the exam, post-exam analysis was quantitative and determined how the questions performed using statistical measurements. ACS Ventures analyzed variables like question difficulty and response options to assess statistical reliability and flagged questions outside target performance ranges.9 Figure 11 provides examples of the types of issues that the analysis flagged. According to ACS Ventures’ post-exam analysis, 40 of the 200 multiple-choice questions on the February 2025 bar exam had statistical performance issues.

Figure 11

Post-Exam Analysis Revealed That the February 2025 Bar Exam Questions Had Statistical Performance Issues

A diagram showing the percentage and number of questions on the February 2025 bar exam that had statistical performance issues.

11 percent, or 23 questions, of the 200 questions had low or negative discrimination. Low discrimination indicates that test takers who performed well on the exam overall performed similarly on the question as those who did not perform well overall. Negative discrimination indicates that applicants who performed well on the exam overall did not perform as well on the question as applicants who scored lower on the exam overall.

Six percent, or 12 questions, of the 200 questions had invalid options. Invalid Options indicates that test takers overall chose only one or two answers for a question, meaning the other answer choices were faulty.

Four percent, or 9 questions, of the 200 questions were too easy.

Seven percent, or 14 questions, of the 200 questions were too difficult. Note: The State Bar identified 18 questions that had multiple performance issues.

Source: The State Bar’s multiple-choice question scoring data.

Note: The State Bar identified 18 questions that had multiple performance issues.

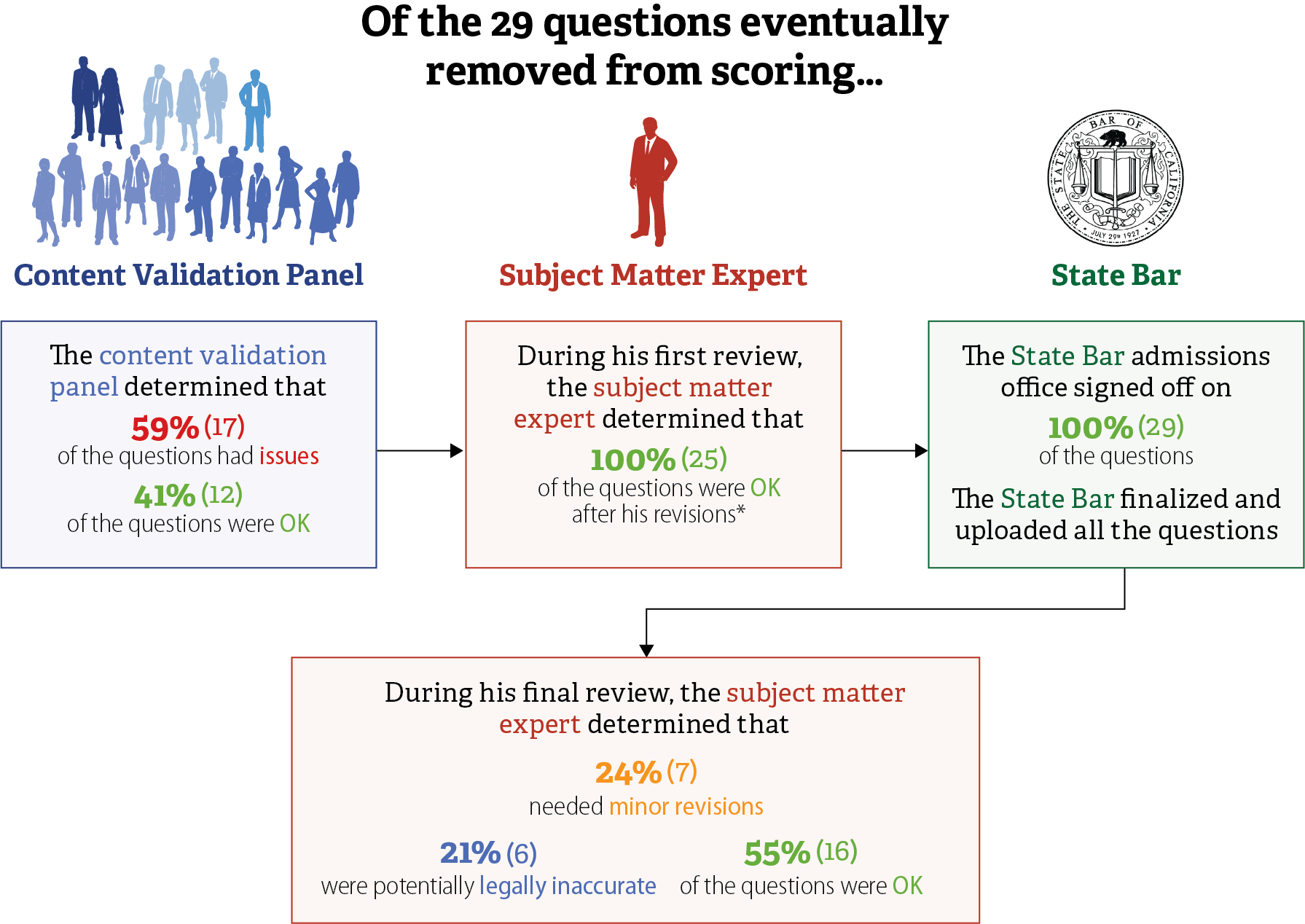

The State Bar retained questions with performance issues for scoring when they did not negatively affect exam reliability and were necessary to maintain adequate subject matter coverage. The State Bar ultimately scored—counted for the purposes of determining test takers’ test scores—19 of the 40 questions that ACS Ventures flagged for performance issues. Maintaining subject matter coverage is essential to bar exam design because the exam must assess core legal concepts to measure a test taker’s ability to apply fundamental legal principles and reasoning across each of the tested subjects and the topics within those subjects. In a 2025 petition to the Supreme Court, the State Bar indicated that including some flagged questions would not materially affect overall examination reliability and could inform revisions for future exam administrations. ACS Ventures’ liaison to the State Bar (ACS Ventures liaison) explained that this course of action maximized content coverage and reliability of the multiple-choice exam.

After ACS Ventures selected 25 questions to remove from scoring, the State Bar removed four more questions than it intended because of concerns about their legal accuracy. Keeping in mind the need for subject matter coverage, ACS Ventures initially selected 175 questions to include in test takers’ scores. Like the NCBE, the State Bar intended to score 175 questions and leave the remaining 25 unscored. However, the State Bar determined it needed to remove more than 25 questions from scoring. After the State Bar informed ACS Ventures that its subject matter expert had identified six questions with potential legal accuracy issues, ACS Ventures reviewed those questions’ performance. During its review, ACS Ventures found that it had already removed two of the potentially legally flawed questions from scoring; it then chose to remove the additional four potentially legally flawed questions, resulting in a total of 171 scored questions. According to the ACS Ventures liaison, there were no well-performing questions from the initial 25 unscored questions that could replace the four potentially legally flawed questions—resulting in 29 unscored questions. As Table 1 shows, questions generated using AI were disproportionately more likely to exhibit performance issues and be removed from scoring. Forty-five percent of questions generated by ACS Ventures were flagged for performance issues and 21 percent were removed from scoring. According to ACS Ventures’ analysis, questions generated using AI also produced difficulty scores that indicated they were comparatively easier for test takers.