2023-101 Santa Clara Valley Transportation Authority

Improvements Are Necessary to Strengthen Its Project Management and Financial Oversight

Published: June 11, 2024Report Number: 2023-101

June 11, 2024

2023‑101

The Governor of California

President pro Tempore of the Senate

Speaker of the Assembly

State Capitol

Sacramento, California 95814

Dear Governor and Legislative Leaders:

As directed by the Joint Legislative Audit Committee, my office conducted an audit of the Santa Clara Valley Transportation Authority (VTA) regarding the agency’s governance structure, project planning and management, financial viability, and fiscal oversight. VTA is a special district that provides transit services throughout Santa Clara County (county). The agency is governed by a Board of Directors (board) consisting of 12 directors who each represent various jurisdictions within the county.

VTA is responsible for planning and delivering improvements to county transit systems or transportation infrastructure. However, the agency needs to strengthen its planning and oversight of such capital projects. For example, when VTA estimates the costs of capital projects, it does not always estimate the cost to operate and maintain the project. Also, VTA’s staff do not provide regular updates to the board about variances from the cost estimates it develops before the construction of a project. For example, the construction cost of one project we reviewed increased by about 24 percent from the start of construction. Without regular information about cost increases such as this one, the board has diminished insight into capital project performance.

The processes for appointing VTA’s directors are not always transparent enough to ensure the appointment of directors with experience in transportation. For example, one group of cities in the county does not meet publicly when it decides who to appoint as its director. Once appointed, VTA’s directors have briefer tenures than those of peer transit agencies, and this is due, in part, to the shorter term lengths that state law establishes for VTA directors compared to the term lengths of other agencies’ directors. As a result, VTA’s board has less experience overseeing the agency’s operations than the boards of peer agencies.

Finally, VTA is in good financial condition but would benefit from adopting additional fiscal oversight practices. More than 60 percent of VTA’s annual revenue comes from sales taxes, which are a time‑limited and uncertain source of revenue. However, VTA has not determined how it will replace this revenue once some of the measures authorizing these taxes begin expiring in 2036. Additionally, VTA’s staff do not report to the board about financial performance metrics, such as the cost per passenger trip, which is information that could assist the board in overseeing VTA’s performance.

Respectfully submitted,

GRANT PARKS

California State Auditor

Selected Abbreviations Used in This Report

| ACFR | Annual Comprehensive Financial Report |

| APTA | American Public Transportation Association |

| BART | Bay Area Rapid Transit |

| CalPERS | California Public Employees’ Retirement System |

| CapMetro | Capital Metropolitan Transportation Authority |

| CEO | Chief Executive Officer |

| CFO | Chief Financial Officer |

| EBRC | Eastridge to BART Regional Connector |

| FPPC | Fair Political Practices Commission |

| FTA | Federal Transit Administration |

| GAO | U.S. Government Accountability Office |

| GFOA | Government Finance Officers Association |

| LA Metro | Los Angeles County Metropolitan Transportation Authority |

| OCTA | Orange County Transportation Authority |

| OPEB | Other post-employment benefits |

| SacRT | Sacramento Regional Transit District |

| SCIP | Strategic Capital Investment Plan |

| SSTPO | Safety, Security, and Transit Planning and Operations |

| TCRP | Transit Cooperative Research Program |

| TriMet | Tri-County Metropolitan Transportation District of Oregon |

| VTA | Santa Clara Valley Transportation Authority |

Summary

Results in Brief

The Santa Clara Valley Transportation Authority (VTA) is a special district responsible for ensuring that Santa Clara County’s (county) transit and transportation needs are met. VTA provides transit services—including light rail and bus service—and traffic congestion management services throughout the county. A 12‑member board of directors (board) governs VTA and sets VTA policy. Board directors are appointed by local elected officials from the city of San José, from the county, and from groups of smaller cities within the county. The head of VTA’s Administrative Branch is the Chief Executive Officer (CEO), who oversees and manages all facets of the organization under policy direction from the board. This audit report concludes the following:

VTA Can Strengthen Its Planning and Oversight of Capital Projects and Better Inform the Board About Cost and Schedule Changes

- VTA addressed individual changes to its capital projects’ costs and schedules in accordance with its procedures. However, VTA’s cost estimates are neither comprehensive nor fully documented. VTA staff also do not regularly report to the board variances in cost or schedule in VTA’s capital projects, leaving the board unaware of important details about these projects and diminishing the board’s oversight of capital projects.

Legislative Changes Could Increase the Transparency and Effectiveness of VTA’s Board

- The process for selecting directors for the board is not always transparent enough to ensure the appointment of directors experienced in transportation issues. For example, the mayors from one group of cities do not meet in public to deliberate regarding whom they will appoint as a director.

- The two‑year term served by VTA’s directors is established in state law and is shorter than the terms of most of their peers at other transportation agencies. In practice, VTA directors have shorter tenures, on average, than their peers, meaning that VTA’s board has less experience overseeing the agency’s operations than the boards of peer agencies.

VTA Should Adopt Several Additional Practices to Optimize Its Financial Health and Strategic Direction

- VTA is in relatively good financial condition. The agency has consistently spent less than it received in revenue, and it has built sizeable reserves to prepare for unexpected financial events. However, VTA relies on an uncertain source—sales taxes—for more than 60 percent of its annual revenue, and it has not yet determined how it will replace this revenue once the measures authorizing these taxes begin expiring in 2036.

- Despite the importance of working from a strategic plan, VTA has been operating with an expired strategic plan since 2022. Further, VTA’s strategic planning documents—the expired plan and a CEO’s list of initiatives—do not contain measurable objectives, strategies for achieving particular objectives, or performance measures that would enable it to track its progress toward achieving its goals.

Agency Comments

VTA agreed with the recommendations we directed to it and indicated that it is committed to implementing them. However, VTA disagreed with the two recommendations we made to the Legislature regarding the transparency of the appointment of directors to its board and the term length for its directors.

Introduction

Background

The Santa Clara Valley Transportation Authority (VTA) is a special district responsible for providing transit services within Santa Clara County (county). VTA reports that it provides transit services to a 346‑square‑mile service area with more than 50 bus routes and more than 50 light rail stations. VTA also serves as the county’s congestion management agency, which means VTA is responsible for developing, adopting, and updating a congestion management program that, among other things, contains traffic level‑of‑service standards for highways and roadways in the county. In these roles, VTA may design and construct state highways, create transit‑oriented joint development projects, and provide bicycle and pedestrian facilities. The text box provides examples of VTA’s responsibilities.

Examples of VTA’s Responsibilities

- Providing public transportation services: bus, light rail, and paratransit.

- Developing countywide transportation planning.

- Managing specific highway improvement projects.

Source: VTA policy.

Structure and Responsibilities of VTA’s Board of Directors

State law assigns responsibility for the governance of VTA to a board of directors (board). The law specifies that the board is composed of 12 members (directors), all of whom must hold office as either a mayor or city council member of a locality within the county, or as a member of the county board of supervisors.1 According to state law, a director’s term on the board may generally last for two years, but the law does not limit the number of terms a director may serve. Figure 1 shows that the directors are appointed from six different regions, or groups, within the county—each having a fixed number of directors.

Figure 1

VTA’s Board Is Composed of Elected Officials From the County and the Cities Therein

Source: State law and VTA’s administrative code.

Each group is responsible for appointing its directors to the board. State law requires that, to the extent possible, the individuals appointed to the board should have expertise, experience, or knowledge relative to transportation issues. For the city of San José (San José) and the county, state law specifies that the city council and the county board of supervisors must appoint their respective directors. However, the law provides that local agreements between the other cities in the county govern how the other directors are chosen. For example, the mayors from the West Valley Cities group appoint that group’s director from a pool of mayors and city council members interested in serving on VTA’s board, whereas the cities in the Northeast Cities group take turns appointing a director to the board, and that choice is approved by the city council of the city assigned the appointment.

Broadly, VTA’s board is responsible for monitoring VTA’s operations and capital projects, as well as setting VTA policy. The text box lists examples of the board’s duties. To assist it in carrying out its responsibilities, the board maintains several standing and advisory committees that are tasked with providing advice and nonbinding recommendations to the board on VTA policy. The board may also form ad hoc committees, composed of directors, to address and resolve specific problems or to achieve defined objectives as needed and for a limited duration. Figure 2 shows the three types of committees.

Examples of the Board’s Responsibilities

- Setting transit rates and charges for the transit services VTA operates.

- Adopting VTA budgets.

- Determining the property and equipment to be owned or acquired by VTA to provide transit services.

- Selecting and evaluating the CEO.

Source: State law; VTA’s rules of procedure; VTA policies.

Figure 2

VTA’s Board Maintains Several Standing and Advisory Committees

Source: VTA administrative code and rules of procedure.

Each standing committee, composed of at least four directors, focuses on a specific area of responsibility. In contrast, advisory committees are composed of individuals who are not directors. Depending on the specific advisory committee, those individuals may be members of the public, organizational representatives, local officials, or a combination of them. Similar to the standing committees, advisory committees exist to offer the board advice and nonbinding recommendations on topics relevant to their areas of responsibility. For example, the Bicycle and Pedestrian Advisory Committee is responsible for providing advice regarding funding priorities for bicycle and pedestrian projects. Committee meeting agendas and documentation show that each standing and advisory committee has a work plan outlining items that the committee intends to address during prospective meetings. However, the board secretary—in consultation with, among others, the board’s chairperson—is responsible for preparing the agenda for full board meetings.

VTA’s Operations and Capital Projects

The head of VTA’s administrative branch is its chief executive officer (CEO), who manages eight divisions. As Figure 3 details, each division carries out different elements of VTA’s responsibilities. VTA’s activities generally fall into two categories: those related to its general operations and those involving capital projects and maintenance. In total for fiscal years 2023–24 and 2024–25, VTA appropriated about $5.7 billion—which included $1.8 billion for operations and $3.9 billion for its capital program. VTA’s operations primarily include the transit services that it provides to its residents—bus, light rail, and paratransit services. VTA’s capital projects and maintenance functions include its efforts to maintain its capital assets in good repair and expand its services by building new infrastructure.

Figure 3

VTA’s Eight Divisions Carry Out Different Functions

Source: VTA’s 2024/2025 biennial budget.

VTA’s Engineering and Program Delivery division is responsible for the development and delivery of various capital projects under VTA’s capital program, including transit and highway projects. Broadly, VTA is responsible for both the delivery and operation of transit projects, therefore it implements and maintains the assets related to transit projects. In contrast, VTA is generally responsible only for the implementation of highway projects, not their maintenance.2 Finally, VTA has a division devoted entirely to the development of one capital project, the Bay Area Rapid Transit (BART) Silicon Valley Extension project.

Other Transit Agencies That We Compared to VTA

Several objectives the Legislature asked us to address as part of our audit led us to identify other transit agencies against which we could compare VTA. Throughout this report, we refer to these as VTA’s peer agencies. We selected five specific entities as peer agencies based on their operating costs, the populations of their service areas, the types of transportation services they provide, and the compositions of their governing boards. Table 1 provides detailed information about these peer agencies and VTA.

Chapter 1

VTA CAN STRENGTHEN ITS PLANNING AND OVERSIGHT OF CAPITAL PROJECTS AND BETTER INFORM THE BOARD ABOUT COST AND SCHEDULE CHANGES

Key Points

- VTA generally followed capital project selection best practices but did not conduct cost‑benefit analyses before selecting two capital projects. As a result, it is not clear whether one of these projects—an extension of VTA’s light rail system—is the best use of the $653 million cost VTA plans to incur.

- VTA did not always estimate the costs of the operation and maintenance of its capital projects when it developed those projects. These estimates are essential to anticipating the expected long‑term costs of the capital projects VTA pursues. Further, the methodologies for VTA’s project cost estimates are only partially documented.

- VTA managed individual changes to project cost and schedule in accordance with its procedures. However, it does not report to the board about deviations from the estimated cost and schedule for capital projects. This lack of reporting diminishes the board’s awareness of important details about these projects.

VTA Did Not Perform Cost‑Benefit Analyses When It Planned Two Major Capital Projects

When transit agencies plan and select capital projects that expand their capacity, the agencies are committing to long‑term, costly efforts with the goal of improving their operations and services. Accordingly, the process such agencies use to plan and select these projects must thoroughly examine the projects across several factors, including an area’s transportation goals and the needs of the community. To assess VTA’s project planning and selection practices, we compared VTA’s processes for two capital projects—the Eastridge to BART Regional Connector (EBRC) and the Silicon Valley Express Lanes Program (express lanes program)—against selected best practices. We selected these projects because they are large projects to which VTA has appropriated funding within the past five years, and they are capital expansion projects, meaning the projects add assets to VTA’s existing system. The text box provides information about the scope of each project. Table 2 summarizes the best practices we reviewed and our determination that VTA followed two of the three best practices for these projects.

VTA Capital Projects Reviewed

Eastridge to BART Regional Connector ($653 million):

VTA plans to build approximately 2.4 miles of light rail track along East Capitol Expressway in San José, starting from its existing Alum Rock station. VTA will build two new light rail stations: an elevated station at Story Road and a ground-level station at VTA’s Eastridge Transit Center. In order to build the light rail track and stations, VTA also plans to remove two existing High-Occupancy Vehicle (HOV) lanes along Capitol Expressway.

Silicon Valley Express Lanes Program ($1.1 billion):

VTA has begun constructing express lanes to add the option for single-occupancy vehicles to pay a toll to use the HOV lanes on certain highways in the county. This program is a multiphase program with multiple projects. Some sections have been collecting toll revenue since 2012. One of the program’s goals is to generate revenue for VTA’s other transit and transportation improvements.

Source: VTA project documents and website.

A key best practice for capital project planning and selection is that an agency implements projects that align with its identified needs. VTA has identified its needs in its Valley Transportation Plan 2040 (VTP 2040). In 2014 the board adopted this plan, which identifies capital programs, projects, and policies that the board plans to pursue through 2040. VTP 2040 outlines VTA’s needs and goals, including accommodating growth in the region, maintaining VTA’s transportation system in a state of good repair, and reducing vehicle miles and hours traveled in order to reduce emissions.

Both projects we reviewed align with needs identified in VTP 2040. Specifically, EBRC’s expected benefits align with VTP 2040’s goals of accommodating population growth, reducing vehicle miles traveled, and reducing emissions. VTA anticipated that the EBRC project will reduce emissions by more than 50,000 metric tons of carbon dioxide and reduce vehicle miles traveled by more than 124 million miles over the span of 50 years. Similarly, the express lanes program helps VTA achieve a different goal specified in VTP 2040: reduced reliance on state and federal funding. VTA expects the express lanes program to generate an average of $164 million per year by 2040—including $68 million per year to fund other transit services and transportation improvements. Additionally, the express lanes will likely continue to operate and generate revenue for VTA beyond the period covered by VTP 2040.

Although the two projects we reviewed are likely to address needs that VTA has identified, VTA’s staff stated that they did not perform a cost‑benefit analysis on either project when they proposed them to the board and received the board’s approval. A cost‑benefit analysis is a tool that transportation agencies use to quantify the benefits to society of implementing a transportation investment and to help determine whether a project is economically efficient. A project is economically efficient if its projected future benefits equal or exceed the project’s life‑cycle costs.

Despite the advisability of using a cost‑benefit analysis to make project selection decisions, VTA did not perform a cost‑benefit analysis that could have informed the selection of these two projects. VTA’s chief engineering and program delivery officer (chief engineering officer) informed us that VTA does not conduct a cost‑benefit analysis on projects unless it is required to do so to obtain external funding because such an analysis takes a considerable amount of staff resources to complete.

However, VTA’s ridership projections for the EBRC project demonstrate the importance of a cost‑benefit analysis because VTA is predicting only a small increase in ridership. We compared the number of riders VTA projects will ride its light rail system in 2043 if it constructs the EBRC project and the number it projects will ride the system if it does not. VTA’s ridership projections show that VTA expects that the EBRC project—which is projected to cost $653 million—will increase light rail ridership by only 1.5 percent by 2043 when compared to the number of riders expected if it did not construct the project. This increase is the equivalent of about 2,500 additional riders per day in that year. The EBRC project’s estimated costs are $272 million per added mile of track. Although a comprehensive cost‑benefit analysis would likely include an examination of more factors than just ridership, such as the effects on greenhouse gas emissions and the effects on the surrounding community, the slim increase in overall ridership is a concerning sign for a project to which VTA is committing significant resources.

In response to these concerns about the EBRC project, VTA’s CEO and its chief external affairs officer asserted that VTA has a commitment to the voters who approved Measure A to follow through on the project. Voters passed Measure A in 2000, and an allowable use of the sales tax revenue generated by that measure is the expansion of light rail into the East Valley region, where VTA plans to construct EBRC. Although the EBRC project is an allowable use of Measure A funds, the measure never required VTA to construct the EBRC project, and the project’s scope does not include all parts of the projects described in the measure. Instead of connecting the East Valley to downtown through a new light rail corridor or through a direct route to downtown, as identified in the measure, the EBRC project adds 2.4 miles of light rail track to the end of an existing light rail line that only indirectly leads to downtown.

Although VTA told us that it generally does not complete cost-benefit analyses, it did conduct some cost‑benefit analyses for the express lanes program. Specifically, its first analysis was for the third phase of the program and occurred 10 years after the board first approved the program and about two years after it made a $28 million appropriation to the third phase. This 2018 analysis demonstrated that this phase’s expected benefits, valued at more than $1 billion, would exceed its costs by $534 million over 10 years. The analyses for the fourth and fifth phases also demonstrated that the phases’ expected benefits would exceed their costs by $50 million over 10 years and $586 million over six years, respectively. VTA completed all three of these analyses using a template issued by the California Department of Transportation (Caltrans). However, VTA did not complete similar analyses for the first two phases of this program. VTA highlighted for us that it had reviewed the feasibility of the express lanes program and secured external financing for the program’s early phases, both of which it believed demonstrated that VTA had performed a review of the program’s value. Although the feasibility study does include a review of the projected expenses and revenues for the program, a project’s estimated direct expenses and resulting revenues are not as thorough as a full consideration of a project’s costs and benefits to society, which would factor in other elements such as emissions and time saved or added to commutes in the region.

As indicated earlier, VTA’s leadership shared that cost-benefit analyses can be costly to produce. More specifically, VTA shared its concern that some of its capital projects are not expected to cost enough to merit a cost‑benefit analysis. For example, VTA pointed out that some capital projects are not major investments that expand transit services but rather smaller, less costly upgrades to existing facilities. One example from VTA’s most recent biennial budget is the remodeling of conference rooms, which is expected to cost only $229,000. We agree that some projects are not costly enough to warrant a cost‑benefit analysis. VTA would likely benefit from establishing a threshold cost to indicate when a project requires such an analysis.

Additionally, the Federal Transit Administration (FTA) and the Federal Highway Administration emphasize the importance of performance measures that help transit agencies assess whether projects are helping the agency meet its goals. VTA performed a comparison between the two projects and relevant transportation performance measures. In its Major Investment Study from December 2000 that aimed to provide a strategy for investing in VTA’s transit system in the Downtown/East Valley region, VTA compared EBRC and other project alternatives against six performance measures. These measures included total riders, new riders, and low‑income households served. The EBRC alternative ranked highest only for the new riders performance measure. Other alternatives—which were bus routes instead of light rail—served more low-income households at lower capital costs but were not supported during community outreach sessions because they ran only during commute hours, whereas EBRC would operate for a greater period of time each day. Because VTA has not yet constructed the EBRC project, it is too early to know whether the project will achieve its expected performance.

VTA also used performance measures to assess its express lanes program. VTA’s Express Lanes Operations Report for fiscal year 2022–23 describes that vehicle speed in express lanes are above the 45 miles‑per‑hour performance goal that VTA adopted from certain federal express-lane standards, showing that the program is succeeding in keeping traffic moving at the speed desired by VTA. The toll systems manager, who oversees express lanes, also provided a variance report demonstrating that for express lanes currently in operation, actual revenue is greater than the amount VTA budgeted. For example, actual revenue for the first three phases of the express lanes program was nearly $7.8 million in fiscal year 2022, whereas VTA had planned for revenue to be less than $6 million.

More recently, VTA began evaluating and prioritizing capital projects by using its Strategic Capital Investment Plan (SCIP). VTA adopted the SCIP in 2022 to help prioritize its long‑term capital needs and identify how it anticipates appropriating funding for its capital projects over the next six years. VTA’s adoption of the SCIP aligns VTA with an FTA recommendation that agencies adopt a standard review and approval framework when determining which projects to select within their capital improvement plans. In particular, VTA staff prioritize a list of proposed capital projects according to weighted scoring criteria, such as increasing ridership, enhancing safety, and environmental sustainability, among other factors. Most factors are assigned a weight of either 15 or 20 percent, with environmental sustainability being granted the lowest weight of 10 percent. Using this list, VTA told us it then ranks the capital projects against additional factors, including financial considerations and board priorities. Staff then use the final list of capital projects in the SCIP to guide the development of the biennial budget, which is how the board appropriates funds for these projects.

Best Practices Can Help Agencies Better Manage Capital Projects’ Costs, Schedules, and Changes

According to the Project Management Institute, project management is the application of knowledge, skills, tools, and techniques to project activities to meet a project’s requirements. The institute explains that project management enables organizations to execute projects effectively and efficiently by helping them resolve problems, manage change, and manage constraints, such as scope, schedule, and costs. A variety of resources—shown in the text box—are available to agencies to guide their project management.

Sources of Project Management Best Practices

- Project Management Institute:

» Project Management Body of Knowledge Guide - Federal Transit Administration:

» Construction Project Management Handbook

» Project and Construction Management Guidelines - Federal Railroad Administration:

» Capital Cost Estimating, Guidance for Project Sponsors - California Department of Transportation:

» Project Development Procedures Manual

» Preparation Guidelines for Project Development Cost Estimates, Cost Estimating Guidelines

» Workplan Standards Guide

» Capital Project Workplan Handbook - U.S. Government Accountability Office:

» Cost Estimating and Assessment Guide - Transportation Research Board:

» Guidebook for the Evaluation of Project Delivery Methods

Source: Auditor research.

Transit and highway projects generally follow the project development process that Figure 4 shows: after initiating a project, agencies design the project, solicit and award the contract, construct the project, and finally close the project and begin its operation and maintenance.

Figure 4

Transit and Highway Projects Follow a General Project Development Process

Source: FTA and Caltrans guidance, interviews with VTA staff.

* Caltrans is responsible for the operation and maintenance of highway projects, with the exception of VTA’s express lanes program.

As part of our audit, we reviewed VTA’s procedures and its implementation of six capital projects—shown in the text box—to determine whether they reflect project management best practices in the areas of cost, schedule, and change control. We focused on these areas at the request of the Legislature and also because they are important areas of project management.

VTA Capital Projects We Reviewed

Rail Rehabilitation Phase 7 (Rail Rehabilitation)—This project is part of an ongoing program to ensure that VTA’s light rail track infrastructure remains in a state of good repair. Rail Rehabilitation includes a subset of four projects:

- Rail Replacement and Rehabilitation FY18 ($20.2 million): The majority of the work includes the repair and replacement of the Younger “Half‑Grand” rail junction, including the installation of two new crossovers.

- Upgrade Ohlone/Chynoweth Interlocking ($4 million): The project includes making improvements to an interlocking at the Ohlone‑Chynoweth light rail station

- Light Rail Crossover and Switches FY16–17 ($8.4 million): The project involves the installation of crossovers and power switches at several locations.

- Rail Replacement and Rehabilitation FY16–17 ($4.5 million): This project includes rehabilitation and replacement of track components at various locations.

Santa Clara Pocket Track (Pocket Track) ($33.6 million): The project included the construction of a pocket track alongside existing track on Tasman Drive.

US 101/De La Cruz Boulevard/Trimble Road Interchange Improvement Project (US 101) ($75.4 million): The project includes various improvements at the US 101 interchange, including the replacement of an existing overcrossing structure over US 101 and the installation of bicycle and pedestrian facilities along De La Cruz Boulevard.

Source: VTA project documentation, VTA’s website, and interviews with VTA staff.

VTA’s Project Cost Estimates Are Not Comprehensive, and Its Cost Estimate Methods Are Not Sufficiently Documented

Project cost estimates are important to agencies as they make investment decisions, set budgets, procure firms to assist with project implementation, and monitor their projects to assess whether they are meeting expectations. Accordingly, it is important for agencies to develop cost estimates that are reliable. The text box shows the four characteristics that the U.S. Government Accountability Office (GAO) Cost Estimating and Assessment Guide states make a cost estimate reliable. The guide also defines each of these traits. For example, a comprehensive cost estimate includes costs from the entire lifecycle of the project, including the operation and maintenance phase, and a credible cost estimate includes a consideration of the project’s risks and the uncertainty around the project. Although the VTA cost estimates we reviewed exhibited some of these characteristics, they fell short in other areas.

Characteristics of a Reliable Cost Estimate

- Comprehensive

- Well documented

- Credible

- Accurate

Source: GAO’s Cost Estimating and Assessment Guide.

For the projects we reviewed, VTA did not address the first of these elements: having comprehensive cost estimates. VTA did not always estimate the operation and maintenance costs for its capital projects as part of its project development, even though operation and maintenance costs are essential to knowing the long‑term costs that an agency will incur by committing to a project. However, for the three projects we reviewed in which VTA expected to incur operation and maintenance costs, the project request forms did not include an estimate of how much those costs would be—instead two of the forms read “TBD,” meaning the costs were yet to be determined. The other form noted that the operation and maintenance costs would be offset by the fare revenue from the project but did not specify how VTA came to this conclusion. Because VTA did not develop operation and maintenance cost estimates for these projects, the agency was at a greater risk of not being prepared to pay for their ongoing costs.

VTA did not estimate operation and maintenance costs at the time of project proposal because it lacked procedures specifying that it should do so. The chief engineering officer confirmed that the Engineering and Program Delivery division does not estimate the operation and maintenance costs for projects and that VTA does not have written procedures for how it develops project cost estimates. He also stated that a separate VTA division estimates project operation and maintenance costs. However, when we spoke with that division and the CEO, neither could clarify the division with this responsibility. Adopting procedures for including operation and maintenance cost estimates could specify which division has responsibility for developing estimates for the operation and maintenance phase of a project. According to VTA, it is in the process of drafting a project administration manual.

The CEO shared that VTA will develop anticipated operation and maintenance costs for substantial projects like EBRC because such estimates are generally required as part of environmental documentation or seeking outside funding. For example, as part of its request for FTA grant funding for BART Phase II, VTA estimated that from fiscal years 2023–24 through 2042–43, VTA’s total direct and fixed overhead operation and maintenance costs for its share of the BART system will be $1.9 billion. Although VTA estimates operation and maintenance costs for substantial projects, it is also important for VTA to develop operation and maintenance cost estimates for the remainder of its capital projects. VTA has a significant number of capital projects. Its 2024–2025 biennial budget included appropriations to 47 capital projects in just its transit capital program, which does not include the substantial projects to which the CEO referred. Therefore, it is important for VTA to understand the operation and maintenance cost implications of its projects, regardless of their size, because without doing so it cannot ascertain the cumulative impact on its financial condition.

We also found that in the projects we reviewed, the second element of a reliable cost estimate was missing: VTA did not fully document its cost estimates. Transportation projects include two key cost estimates, which the text box shows. In addition to the GAO guidance we discuss above defining a reliable cost estimate, guidance from the FTA, Federal Railroad Administration, and Caltrans also indicates that a well‑developed cost estimate is documented, traceable, and includes documented assumptions the agency used to create the estimate.

Two Key Cost Estimates of Transportation Projects

Initial Cost Estimate—Referred to as “conceptual” or “order‑of‑magnitude” estimates. These estimates are developed when a quick estimate is needed and few details are available.

Baseline Cost Estimate—The control budget against which project cost performance is measured and change is controlled.

Source: FTA and the GAO.

However, VTA’s documentation of its project cost estimates are not always aligned with this guidance. The documents we reviewed for VTA’s initial cost estimates showed a reasonable explanation for the estimates that VTA developed given the nature of the cost estimate. As the text box indicates, the initial cost estimate is a rough order‑of‑magnitude estimate, so we did not expect VTA to keep detailed documentation to explain how it arrived at this estimate. VTA does not use the term baseline to refer to any of its cost estimates. Nonetheless, we observed that it treats its preconstruction cost estimates as baseline estimates. Preconstruction cost estimates are those cost estimates that VTA has developed by the time it has fully designed the project and awarded the construction contracts. To determine whether VTA documents its more developed project cost estimates, we reviewed VTA’s preconstruction cost estimates, as the FTA indicates that an agency should establish a baseline cost by that point in the project process.

Although the preconstruction estimates we reviewed were composed of several different types of work on the project, including design, construction, and other costs, VTA could provide documentation of its methodology for only some of these costs. VTA provided us with the documented estimation methodology for the construction portions of the projects. VTA also provided some documentation for the design portions of the six projects we reviewed, but this documentation was not comprehensive across all of the projects. Specifically, VTA provided documentation of its design cost methodology for the majority of the design costs for the Rail Rehabilitation projects and the US 101 project. However, VTA had only partially documented its methodology for the Pocket Track project. VTA had documented its estimates for the design and construction portions of these projects because it needs that information when it enters into contracts, which it uses to hold contractors responsible for the costs of specific services.

However, VTA’s project managers did not consistently retain documented methodologies for the development of other costs for its projects—that is, the costs not related to designing and building the project, such as fees, testing, and third‑party costs. For example, the engineering group manager for VTA’s highway program and the US 101 project manager confirmed that there was no documented methodology for the utility relocation and field operation costs for the project because they are placeholder estimates. Also, although VTA uses a staffing spreadsheet to estimate its own labor costs, it did not always keep copies of these spreadsheets. Among the six projects we reviewed, VTA had maintained complete documentation of labor estimates for only one project and retained partial documentation for another. Among the projects we reviewed, the magnitudes of the costs incurred without documented methodologies in relation to the overall project costs ranged from 13 percent to 38 percent.

VTA’s deputy director of construction for transit engineering (construction deputy director) confirmed that VTA does not require its project managers to document the methodology used to develop their preconstruction estimates because it expects project managers to already have the technical expertise to create an estimate as part of their job qualifications and responsibilities. The GAO notes that undocumented cost estimates can lead to unanswerable questions about the estimate and make it harder for others who are unfamiliar with the project to use the estimate effectively. Furthermore, the lack of documentation creates difficulty when trying to conduct analyses of why actual costs differed from the estimates. By not requiring its staff to document their assumptions, VTA is at a higher risk for these effects.

Because VTA’s cost estimates were partially undocumented, VTA cannot know how credible they are and therefore how well they align with the third element of a reliable cost estimate. The GAO states that credible cost estimates are developed with consideration for the sensitivity of the estimates’ assumptions and the risks of the project. The GAO suggests that agencies develop estimates that help decision makers appreciate the range of costs that a project may incur so they can make informed decisions about the project. However, the cost methodology documents VTA provided during this audit did not show VTA had identified a range of costs or demonstrate the effects of changing assumptions. Nevertheless, we note that for the construction portions of the projects we reviewed, VTA compared its own estimate of costs against the estimates provided by bidders, which provides some independent validation of costs.

Finally, although VTA’s cost estimates are incomplete, they were generally accurate for the phases of the project that they covered. For the costs it does estimate, VTA has provided its board with a schedule of expected accuracy for its cost estimates, with the degree of accuracy dependent on the state of a project’s design. Table 3 shows VTA’s expected accuracy ranges for the initial and preconstruction estimates.

The majority of the cost estimates for the projects we reviewed—10 of 12 estimates—fell within the expected accuracy ranges. The most significant outlier was the initial estimate for the Upgrade Ohlone/Chynoweth Interlocking project. The actual costs for this project were close to 300 percent higher than VTA’s original cost estimate. According to documentation requesting the budget increase, the affected project area was larger than originally planned, and VTA did not anticipate the extensive system changes and equipment required to complete the project.

VTA Generally Followed Best Practices for Developing Its Project Schedules

Another key activity within project management is the development and management of an accurate and complete project schedule. According to the FTA, a schedule is one of the tools that project managers use to maintain accountability for the activities that take place during a project, anticipate upcoming activities, review progress, and modify work plans if necessary. The FTA’s publication Project and Construction Management Guidelines provides examples of the different types of schedules that transit projects typically include. Among these is the Integrated Master Project Schedule (master schedule), which FTA advises should be developed early in the project lifecycle and should include information from all phases of the project lifecycle up to, but not including, the operation and maintenance phase. However, to build the master schedule, agencies must first define the specific actions necessary to produce the project’s deliverables and then estimate the amount of time necessary to complete those activities.

Consistent with best practices, for the six projects we reviewed, VTA defined the specific project activities necessary to produce deliverables and estimated the duration of each activity. For example, VTA noted that specific actions, such as writing a memo to the board and obtaining board authorization to proceed, must happen before it could award the construction contract for the US 101 project. VTA also developed the estimated start and finish dates and the estimated number of days each activity would take. By following the advised scheduling practices, VTA helps ensure that it is developing detailed schedules that will more accurately reflect the time it will take to complete a project.

In addition, VTA met industry best practices and developed a master schedule for the projects we reviewed. FTA notes that a master schedule is the official project schedule and should display how the project will be logically implemented. According to VTA’s project schedule guidelines, VTA’s project manager or project controls unit prepares a draft master schedule upon initiating a project. In the projects’ master schedules, we found that VTA included all project phases from inception to closeout, including design and engineering, bid and award, and construction. Because VTA implements master schedules, it ensures that it is developing a detailed overview of the project schedule that it can manage during the project.

Similar to our cost estimates review in the previous section, we calculated the variances between VTA’s schedule estimates and its actual project timelines. Table 4 shows the variances for VTA’s initial and preconstruction estimates for the projects we reviewed. The variances were in part the result of circumstances outside of VTA’s control. For example, according to the project change orders, extensions to the Rail Rehabilitation schedule during the construction phase were caused in part by global supply chain issues and a May 2021 shooting incident at a VTA rail yard. Also, the project manager for the US 101 highway project shared that the design consultant developed an ambitious schedule for the project’s design, but stakeholders such as Caltrans, the city of San José, and the Federal Aviation Administration took longer than expected to review the design of the project.

VTA Does Not Regularly Report Project Variances to the Board

The FTA and the Project Management Institute both advise that a project sponsor, such as VTA, have a process for managing changes to contracts that increase the cost, schedule, or scope of the project. The FTA explains that a change control process can enable decision‑makers to make cost‑effective decisions and help oversight staff identify errors as the source of the needed change. VTA’s change management guidelines detail its process for managing changes to its construction contracts (change control process). That process includes documenting the following: the justification for any change, the effect on the project’s cost and schedule where applicable, a cost analysis, a record of VTA’s negotiation with the contractor, and approval by the change control board. The package of documents in which VTA presents these factors is called a change order, and each change order that changes the contract value by more than $50,000 or changes the contract’s schedule must be approved by VTA’s change control board. The change control board includes senior VTA staff and is responsible for reviewing and approving contract changes to ensure that, among other requirements, they are appropriate, necessary, and include required documents.

We examined a selection of 19 change orders that affected the costs or the schedules for construction contracts related to the six capital projects we reviewed. We found that VTA followed its procedures for handling these change orders, including obtaining approval from the change control board. Consistent with VTA’s change management guidelines, the change orders we reviewed contained justifications for the changes, descriptions of the change orders’ effect on the schedules where applicable, cost analyses, records of negotiation, and approval by the change control board.

For example, VTA required a change order related to the Pocket Track project to account for lost productivity due to multiple factors, including design changes. These changes increased the cost of that particular construction contract, which had an original value of $13.7 million and had already undergone $1.6 million in prior contract changes, by another $1.7 million. The project documentation for the related change order contained the required elements, including a description of the justification for the changes and a detailed discussion of the negotiations with the contractor on the price of the changes.

VTA’s staff also regularly monitor project cost and schedule information. Guidance from the FTA prescribes that agencies should monitor project costs and schedules through frequent reporting to management of the projects’ approved and ongoing costs, as well as schedule progress. We reviewed VTA’s capital project documentation and determined that VTA follows this guidance through various reporting and monitoring methods. For example, VTA utilizes monthly cost reports that monitor and report to VTA management cost information, such as the projects’ approved budget, estimated total costs, and incurred costs. Also, VTA’s technical services group manager told us that project managers and schedulers review and update project schedules on a monthly basis. Further, a deputy director of construction told us that every quarter he, the chief engineering officer, and VTA’s project controls unit, review transit project cost and schedule information. We reviewed examples of the project reports that the managers evaluate at these meetings and verified that the reports show project cost and schedule information along with the current project phase.

However, VTA staff do not regularly inform the board about project cost or schedule variances. VTA’s staff provide updates to the board about capital project budgets and funding levels in the biennial budget. For example, the budget includes information about total capital project costs, unspent funds, and funding sources for each project. However, VTA staff confirmed that it does not regularly update the board about variances in capital projects from the preconstruction estimates. For example, earlier in this section we discussed a change order to a construction contract originally worth $13.7 million. Cumulatively, as of the change order that we reviewed, the cost of that contract had grown to about $17 million, or about a 24 percent increase. Because VTA staff do not regularly inform the board about variances such as this one, the board’s understanding of capital project performance is diminished.

In response to our concern that staff do not provide the board with updates about variances from the preconstruction estimated costs and schedule for VTA’s capital projects, the staff liaison to VTA’s Capital Program Committee agreed that there would be value in staff providing semiannual reports to that committee and the board. The staff liaison indicated that the reports should include updates comparing the cost and schedule estimates of capital projects at contract award to their actual cost and schedule for any projects that have had a material change to either factor. The staff liaison stated that he was unaware of a reason the board does not receive semiannual reports of capital projects but added that these reports would improve the board’s understanding and management of VTA’s capital programs.

Recommendations

To ensure that VTA’s board is fully informed when approving projects, VTA should update its planning procedures by December 2024 to do the following:

- Establish a threshold for estimated project cost that defines when project planning must include the performance of a cost‑benefit analysis.

- Conduct a cost‑benefit analysis for all capital projects that meet or exceed that cost threshold.

To help ensure that it develops reliable cost estimates for its capital projects, VTA should develop procedures by December 2024 to do the following:

- Document the methodology for developing its capital project cost estimates, including costs other than those directly related to the design and construction of the project.

- Estimate the anticipated operation and maintenance costs for capital projects in development.

To help ensure that the board can monitor project costs and schedules, VTA should develop procedures by December 2024 to monitor project costs and schedules against preconstruction estimates and present this information as part of its semiannual report to both the Capital Program Committee and the board. This report should provide status updates on the agency’s existing capital projects and identify deviations from projects’ preconstruction estimates.

Chapter 2

LEGISLATIVE CHANGES COULD INCREASE THE TRANSPARENCY AND EFFECTIVENESS OF VTA’S BOARD

Key Points

- The 12 directors on VTA’s board are elected officials who are chosen by elected officials, which makes the board similar to other transit boards. However, the director selection process is not always transparent enough to ensure the appointment of directors experienced in transportation issues.

- VTA directors have shorter terms than their peers on other transit boards, which leads to shorter tenure overall, lessening the overall experience level on the board.

- The board generally uses both its standing committees and advisory committees effectively to review policies and make recommendations to the full board.

- Although VTA has safeguards in place to ensure that directors adhere to their fiduciary duties, it should make improvements to promote accountability for financial interest disclosures and ethics training.

VTA’s Director Selection Process Is Not Transparent Enough to Ensure the Appointment of Experienced Directors

The 12 VTA directors are public officials responsible for the strategic direction of VTA. Their decisions can affect the quality of life of everyone who lives within VTA’s jurisdiction. Given the public nature of their positions and the degree of influence that directors have, it is important that, whenever possible, directors are individuals with experience in or knowledge about transportation. To assess VTA’s process for selecting and appointing directors, we considered three factors: who selects the directors, who is eligible to serve as a director, and the selection approach used by those who select directors.

Specific elected officials appoint VTA’s directors, a practice that makes VTA similar to other transportation agencies. State law requires the San José City Council to appoint the city’s VTA directors and the Santa Clara County Board of Supervisors to appoint the county’s directors. Further, state law specifies that agreements between the remaining cities in the county govern how their directors are chosen. We determined that as of December 2023, the directors that represent cities other than San José were appointed by elected officials. State law refers to those responsible for making appointments to the VTA board as appointing powers. We reviewed the appointments of each voting director as of December 2023, and determined that all were selected by the appropriate appointing powers.

Having elected officials appoint directors aligns VTA with the most common practice in the country. According to the American Public Transportation Association (APTA), 60 percent of transit boards are appointed by local or state officials, such as mayors, governors, or a legislative body, and only 3 percent of transit boards are directly elected.3 The laws that create four of the five peer agencies we reviewed also specify that certain elected officials, such as city council members, mayors, and county supervisors, appoint all but three of the directors of those agencies.4 VTA not only conforms to the most common practice nationwide but also has a practice similar to its peers.

State law restricts who can serve as a director and, within those restrictions, VTA has provided guidance to the appointing powers about the desirable traits for a director. As the text box shows, state law does not allow a member of the general public to serve as a VTA board director. Additionally, state law requires that, to the extent possible, directors be individuals with expertise, experience, or knowledge relative to transportation issues—a requirement we refer to in this report as the experience requirement. As of December 2023, all directors were the elected officials state law requires. However, as we note in more detail below, the appointing powers did not always demonstrate to the public that they fulfilled the experience requirement when appointing directors. In addition to the requirements in state law, VTA has published nonbinding guidance for the appointing powers about its expectations for directors. These expectations include the directors devoting an average of five to 10 hours per month to board and committee assignments, representing the interests of their constituency while endeavoring to achieve regional consensus, and keeping their respective jurisdictions informed on key issues.

Requirements for VTA Director Selection

- Directors appointed by a city must be a mayor or city council member, and directors appointed by the county must be a member of the board of supervisors.

- To the extent possible, appointing powers must select directors who have expertise, experience, or knowledge relative to transportation issues.

Source: State law.

The state law requiring that VTA’s directors are specified elected officials is unique among the peer agencies we reviewed. The law that establishes SacRT does not restrict directorship to elected officials, although in practice the board—as of April 2024—is composed solely of city council members and county supervisors. Differently, the state law that governs CapMetro requires that three of its eight directors be elected officials but does not restrict the other five directorships to elected officials. In addition, the board of directors for LA Metro and OCTA are required by law to be composed of a combination of members of the public and specified elected officials, with the majority of directors on each board required to be those elected officials.

Restricting directorships to elected officials likely provides some benefits, but the practice also limits the expertise that appointing powers can access when making appointment decisions. In our July 2008 audit of VTA, we stated that having elected officials serve on the board may allow VTA to be more influential in aligning local land use decisions with the countywide transportation plan.5 Additionally, elected officials—having gained support for their leadership—could serve as trusted messengers to their local jurisdictions on behalf of VTA. Nonetheless, because state law restricts other individuals from serving as directors, the pool of candidates for VTA’s board is limited and excludes members of the public who have direct experience with transit or transportation issues. Overall, the law limiting directors to specified elected officials likely leads to a board with less experience with transit or transportation issues than one that could exist without such limits.

Nonetheless, the appointing powers could maximize the transit and transportation experience on the board by ensuring that their appointments comply with the experience requirement. Accordingly, we reviewed the ways in which a selection of appointing powers chose their directors to determine whether the appointment processes were public and demonstrated that the appointing powers complied with the experience requirement. Specifically, we reviewed the available public record of the meetings for the appointing powers that took place in January and February 2023, as presented in Figure 5.6

Figure 5

The Appointing Powers We Reviewed Have Different Processes for Selecting Directors

Source: State law and VTA administrative code; documentation and interviews provided by each city group.

Note: The graphic does not include the selection processes for Santa Clara County, Gilroy, Morgan Hill, Los Altos, Los Altos Hills, Mountain View, or Palo Alto.

None of the appointing powers we reviewed have a formal process that requires them to publicly cite and document appointee qualifications. This lack of a formal public process may allow the appointing powers to circumvent the experience requirement. For appointments made by the cities of San José, Sunnyvale, and Santa Clara, the appointments were made at a public city council meeting. The city councils for San José and Sunnyvale discussed the general attributes of their appointees, including experience and the ability to work with others. For example, in January 2023, Sunnyvale’s city council discussed its appointee’s experience serving on VTA’s policy advisory committee and the benefits that experience would provide to the individual as a director.

However, each of the appointing powers confirmed that it does not have a formal process to make public the qualifications of its appointees to VTA’s board. As a result, appointing powers are able to make appointments without having affirmatively demonstrated to the public that their appointees have the relevant experience necessary to fulfill their responsibilities on VTA’s board. For example, during Santa Clara’s city council meeting in February 2023, it voted to approve the appointment of its VTA director without any discussion of that individual’s qualifications or the extent to which it had considered other candidates who may have had transportation experience. Without a process in place requiring appointing powers to make public the qualifications of their appointees, VTA and the public are not always able to determine whether the appointing powers adhered to the experience requirement and appointed qualified candidates to VTA’s board.

The remaining cities we reviewed—Campbell, Cupertino, Monte Sereno, Saratoga, and the town of Los Gatos—which represent a single city group, used the least transparent appointment process among the groups we reviewed. This process involves the mayors or other designated leaders of each city holding a meeting to determine who will be their appointed director. State law governing local government meetings requires that legislative bodies of local agencies—such as city councils—publicly report all actions taken by the body. However, this appointing power is not a legislative body and, as a result, it is not required by this law to hold a public meeting. Campbell’s city manager confirmed that this appointing power’s meeting is not public. Accordingly, the public does not know this group’s reasons for its appointment decisions and has no assurance that the appointing power satisfied the requirement to appoint individuals with transportation experience to the extent it was possible to do so.

Because appointment decisions are not always deliberated and delivered in public, a significant safeguard for ensuring that appointing powers choose qualified directors is missing. VTA’s CEO agreed that the appointing powers should be more transparent in the selection of their directors, but she also expressed her belief that VTA’s enabling statute did not need to be amended to promote such transparency. Nonetheless, because VTA does not have the authority to mandate such transparency, legislative action would be required to compel more transparency in the appointment process.

VTA Directors Have Briefer Tenures Than Their Peers at Other Transit Agencies

Although we could not identify any recommendations from authoritative sources specifying the number of years that a director should serve on a board of directors, we reviewed available guidance on board membership in the public sector and determined that having a mixture of experience levels on the board can provide benefits. For example, the California State Teachers’ Retirement System’s governance guidance states that effective boards have both short‑ and long‑tenured directors to ensure that fresh perspectives are provided and that experience, continuity, and stability exist on the board.

The Transit Cooperative Research Program (TCRP)—a federally sponsored transportation research organization—reported that in response to a national survey of transit CEOs and board chairs, respondents said that some of their board members serve staggered terms to ensure that the board has both continuity and fresh ideas. The TCRP further reported that transit agency boards should have sufficient continuity and institutional memory to promote long‑term planning and follow‑through. These sources indicate that longer‑tenured directors can benefit a board by providing stability and experience.

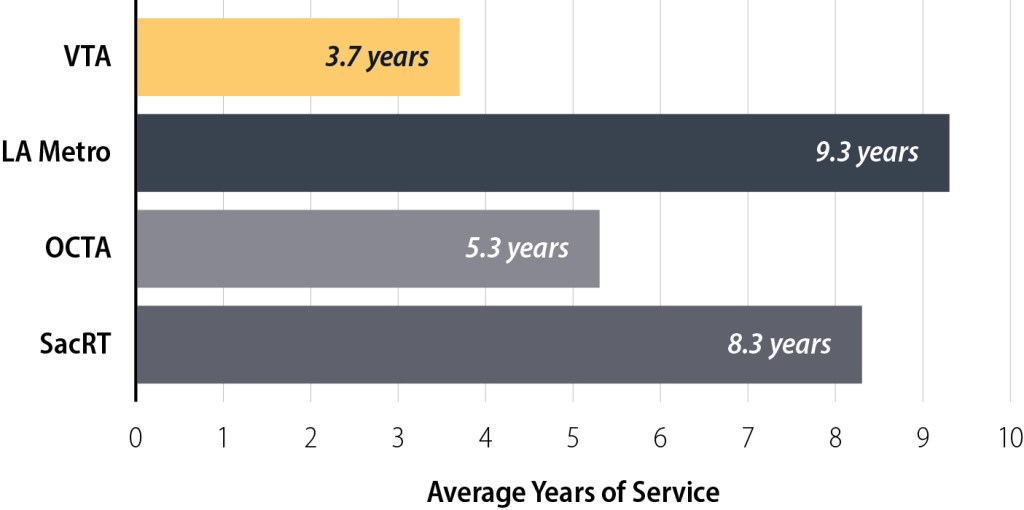

However, the average tenure of VTA’s directors is shorter than directors’ average tenure at the peer agencies we reviewed. Only three of the peer agencies—LA Metro, OCTA, and SacRT—maintained historical data regarding their directors’ tenures. To assess the average tenure of directors at VTA and at these agencies, we identified all directors who served for any duration during the period of 2013 through 2023. We then calculated the average number of years those directors served regardless of when those years occurred. Figure 6 shows the results of our review and demonstrates that VTA’s directors served for notably shorter periods, on average, than did their peers.

Figure 6

VTA Directors’ Average Tenure Is Shorter Than Average Tenures of Directors at Peer Agencies

Source: Director tenure documentation provided by the agencies that maintain such data.

Note: CapMetro and TriMet did not maintain historical data on the tenure of their directors.

One contributing factor to shorter tenure among VTA’s directors is VTA’s shorter term lengths. As we describe in the Introduction, state law establishes the term length for VTA’s directors generally at two years. State law allows up to 30 days beyond two years if a director’s successor has not been appointed. However, this term length is generally half as long as the duration of the term lengths among VTA’s peers. Three of the five peer agencies have four‑year terms. Table 5 compares the term lengths of VTA directors and those of its peers. VTA’s term lengths are also shorter than the national average. According to the TCRP, the average transit board member serves a three‑year or four‑year term.

Another factor contributing to VTA’s shorter director tenures has been the city groups’ appointment decisions. Directors who were appointed by the city groups that have only one board director representative as well as the Northeast Cities group all had shorter tenures than the directors representing San José and the county, who had average tenures of roughly four and eight years respectively. The state law that creates VTA does not establish a limit on the number of terms that a person can serve as a VTA director—meaning that so long as a person continues to serve as an eligible elected official in their respective jurisdiction, a city group could reappoint that individual as their designated director indefinitely. In fact, the South County group, composed of Gilroy and Morgan Hill, has reappointed individuals to consecutive terms, resulting in that group having directors with the longest average tenure of any of the non‑San José city groups at an average of nearly three‑and‑a‑half years. The remaining non‑San José city groups have generally rotated which cities appoint a director to the board, and those directors have an average tenure of about two‑and‑a‑half years. Although that practice allows for the city groups to rotate which city has a director on the board, it generally detracts from the overall tenure and experience level of the board.

In previous reviews of its board tenure, VTA has received recommendations to extend its term length to four years. Our July 2008 audit found that VTA director tenure was shorter than tenures at comparable transit agencies at that time, and we recommended that VTA request a change to state law that would allow it to implement a four‑year term. Similarly, a 2019 grand jury review of VTA noted that extending the term length of its directors to four years would increase the average tenure of board members and help provide continuity on the board. In May 2019, a VTA ad hoc board enhancement committee began meeting to review VTA’s governance practices. This committee commissioned an independent study that ultimately recommended that VTA’s board adopt a four‑year term for its directors.

Despite these recommendations to pursue a four‑year term length for its directors, VTA has not done so. In response to our July 2008 recommendation, VTA stated that the board had recently voted to keep a two‑year term for its directors and encouraged the appointing powers to reappoint board members to consecutive terms. A VTA staff report in August 2020 to the Governance and Audit committee in response to the 2019 study of VTA’s structure reached similar conclusions. Although staff noted that it takes a VTA director about two years on average to become comfortable and effective in their role, the staff recommended that VTA keep the two‑year term length. The staff report noted that the two‑year term length allowed city groups to remain flexible with their appointments, whereas a four‑year term can limit their flexibility and options.

Because state law establishes the length of VTA’s directors’ terms, legislative action will be necessary to lengthen those terms. In July 2008 our office reported that extending the terms to a four‑year period was appropriate and recommended that VTA pursue this change to the law. Nearly 16 years have passed since we made that recommendation, and VTA’s tenure remains lower than its peers. Therefore, we believe that the Legislature should take action to extend the term length for VTA directors to four years, more closely aligning VTA with its peer agencies and helping to ensure that it is composed of individuals with the experience to lead VTA.

VTA’s Use of Alternate Directors Does Not Lower the Attendance of Regular Directors

When directors cannot attend a board or committee meeting, VTA uses alternate directors to attend the meetings in their absence. According to state law, in addition to the 12 directors, there must be two alternate directors, one from the county and one from San José. Further, state law permits the other cities to agree to have alternate directors. VTA’s administrative code states that alternate directors will attend board meetings, attend assigned standing committee meetings, and sit for and vote in place of their director if that director is absent. Alternate directors are not required to attend board meetings unless the director they are an alternate for cannot attend, although they are allowed to attend even when the director they serve as an alternate for is already in attendance.

We also reviewed guidance from the TCRP on board governance and management of transit agencies. The guidance noted that boards may use alternate directors; however, the guidance we reviewed neither recommended nor discouraged the practice. Of the five peer agencies we reviewed, only SacRT uses alternate directors. The law establishing SacRT allows the entities appointing directors to the board to also select alternate directors.

External reviewers have expressed concern about VTA’s use of alternate directors. In 2019 the Santa Clara County Civil Grand Jury released a report on VTA’s governance and remarked that alternate directors may cause directors to deprioritize meeting attendance. Also in 2019, VTA contracted for a governance assessment, and the scope of work included evaluating VTA’s governance compared to other transit agencies. The firm that conducted the assessment recommended that VTA stop using alternate directors, stating that the alternate directors are often not needed to achieve a quorum and their average attendance rate is low—indicating that the board often does not rely on the alternates.

However, the existence of alternate directors does not appear to have affected director attendance, which was generally high. We reviewed VTA director attendance data from 2020 through June 2023. VTA directors attended 92 percent of board meetings and 83 percent of committee meetings, which are relatively high attendance rates. Further, VTA staff and directors noted that there is value in having alternate directors, including the fact that serving as an alternate director can provide experience and exposure to VTA that could prepare an alternate to become a director. In our review of board tenure we noted that several directors who served during the past ten years had started as alternates. Given the relatively high attendance rate of regular directors and the potential benefits of alternate directors, we did not conclude that VTA should discontinue its use of alternate directors.

VTA’s Board Generally Uses Its Committees Effectively by Consulting Them About Relevant Policies and Incorporating Their Input

As we describe in the Introduction, VTA maintains several standing and advisory committees. VTA’s administrative code, rules of procedure, and committee bylaws assign a title, duties, and responsibilities to each committee. For example, the Capital Program Committee is responsible for reviewing and recommending to the board policies pertaining to VTA’s capital projects. According to the TCRP, transit agencies create committees to accomplish specific tasks and to address needs that the board is responsible for governing. The TCRP adds that committees make recommendations to the full board for approval. To assess whether VTA uses its committees effectively, we reviewed each standing and advisory committee’s involvement in the development of five VTA policies, which the text box lists. For each policy, we assessed three areas: whether all of the applicable standing and advisory committees provided their perspective or advice on the policy, whether the committees provided that perspective or advice before board approval, and whether VTA staff presented the committees’ perspective or advice to the board.

Policies We Reviewed for Board Committee Involvement

- Biennial budget for fiscal years 2024–25 and 2025–26

- Strategic Capital Investment Plan

- Visionary Transit Network Plan

- 2023 Transit Service Plan

- 2016 Measure B 10-Year Program and Biennial Budget Principles.

Source: VTA policies.

For the five policies we reviewed, the board’s committees generally reviewed the policies and provided advice or recommendations when the policies were relevant to the committees’ areas of responsibility. For example, the Capital Program Committee reviewed and provided advice on VTA’s Strategic Capital Investment Plan (SCIP), but it did not review the 2023 Transit Service Plan, which was outside of the committee’s purview because it focused on changes to VTA’s services rather than its capital programs.

In total, across the five policies we reviewed and VTA’s 10 standing and advisory committees, we identified 34 instances in which a committee’s responsibilities appeared to overlap with the policies we reviewed. In all but eight of these cases, VTA’s committees reviewed the relevant policy. In four of these eight cases, VTA had reasonable explanations for why the apparently relevant committees did not review a particular policy. One example of this type of exception is the approach VTA took to review its biennial budget. Although the Safety, Security, and Transit Planning and Operations (SSTPO) Committee is responsible for making recommendations to the board about transit planning, capital projects, and operations and marketing, it did not review the biennial budget. However, the staff liaison to this committee explained that, although the biennial budget allocates funds for transit projects and operations, the committee did not review the budget because it does not relate to the planning or development of projects with respect to their safety or security—which is a focus of the committee’s responsibilities. We find this explanation reasonable.

Nevertheless, we found four instances in which committees likely should have reviewed a policy but did not do so. As mentioned above, the Capital Program Committee reviewed the SCIP, but no advisory committees reviewed that policy. According to the staff liaison for the committee, VTA chose to focus the involvement of its standing committees to just the Capital Program Committee because it is the committee with primary responsibility for this plan and doing so alleviated the workload of the other committees. We agree that this rationale is reasonable but note that it meant two advisory committees—the Policy Advisory Committee and the Technical Advisory Committee—did not review the SCIP when they likely should have given their purviews. For example, the Policy Advisory Committee—which is made up of members who represent VTA’s member cities—is responsible for advising the board on multiple issues, including long‑range transportation planning, VTA’s budget, and service modifications, and as a result could provide valuable stakeholder input on the SCIP. The staff liaison agreed that it was a good idea for VTA to solicit stakeholder input on the SCIP and that, looking forward, VTA should present matters regarding the SCIP to relevant advisory committees.

In addition, we found two other instances in which a committee was not involved in a policy related to its responsibility. Specifically, the Bicycle and Pedestrian Advisory Committee, which is responsible for providing advice to the board on funding priorities for bicycle and pedestrian projects, did not review the program principles that guide funding for the 2016 Measure B Program—a program that in part funds bicycle and pedestrian projects of countywide significance—for a 10‑year period. The committee’s staff liaison acknowledged that not involving the committee was an oversight by VTA’s staff. Similarly, the Capital Program Committee also did not review the principles for the 2016 Measure B Program, which funds capital projects that are in part managed by VTA. As a result, the committee missed an opportunity to fulfill its responsibility to review the efficacy of a policy that influences how the agency intends to fund VTA capital projects.